重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

A. is

B. have

C. be

D. arise

更多“Should there()any complaint from the end users, please let us know.A. isB. haveC. beD.”相关的问题

更多“Should there()any complaint from the end users, please let us know.A. isB. haveC. beD.”相关的问题

第1题

(b) The chief executive of Xalam Co, an exporter of specialist equipment, has asked for advice on the accounting

treatment and disclosure of payments made for security consultancy services. The payments, which aim to

ensure that consignments are not impounded in the destination country of a major customer, may be material to

the financial statements for the year ending 30 June 2006. Xalam does not treat these payments as tax

deductible. (4 marks)

Required:

Identify and comment on the ethical and other professional issues raised by each of these matters and state what

action, if any, Dedza should now take.

NOTE: The mark allocation is shown against each of the three situations.

第2题

specific responsibility for undertaking annual reviews of existing clients. The following situations have arisen in

connection with three client companies:

(a) Dedza was appointed auditor and tax advisor to Kora Co, a limited liability company, last year and has recently

issued an unmodified opinion on the financial statements for the year ended 30 June 2005. To your surprise,

the tax authority has just launched an investigation into the affairs of Kora on suspicion of underdeclaring income.

(7 marks)

Required:

Identify and comment on the ethical and other professional issues raised by each of these matters and state what

action, if any, Dedza should now take.

NOTE: The mark allocation is shown against each of the three situations.

第3题

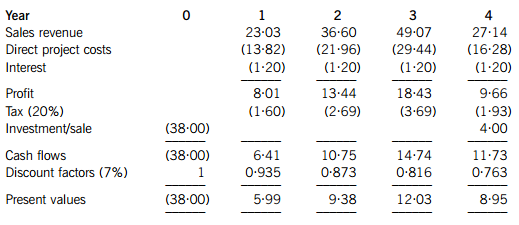

Section B – TWO questions ONLY to be attempted

You have recently commenced working for Burung Co and are reviewing a four-year project which the company is considering for investment. The project is in a business activity which is very different from Burung Co’s current line of business.

The following net present value estimate has been made for the project:

All figures are in $ million

Net present value is negative $1·65 million, and therefore the recommendation is that the project should not be accepted.

In calculating the net present value of the project, the following notes were made:

(i) Since the real cost of capital is used to discount cash flows, neither the sales revenue nor the direct project costs have been inflated. It is estimated that the inflation rate applicable to sales revenue is 8% per year and to the direct project costs is 4% per year.

(ii) The project will require an initial investment of $38 million. Of this, $16 million relates to plant and machinery, which is expected to be sold for $4 million when the project ceases, after taking any taxation and inflation impact into account.

(iii) Tax allowable depreciation is available on the plant and machinery at 50% in the first year, followed by 25% per year thereafter on a reducing balance basis. A balancing adjustment is available in the year the plant and machinery is sold. Burung Co pays 20% tax on its annual taxable profits. No tax allowable depreciation is available on the remaining investment assets and they will have a nil value at the end of the project.

(iv) Burung Co uses either a nominal cost of capital of 11% or a real cost of capital of 7% to discount all projects, given that the rate of inflation has been stable at 4% for a number of years.

(v) Interest is based on Burung Co’s normal borrowing rate of 150 basis points over the 10-year government yield rate.

(vi) At the beginning of each year, Burung Co will need to provide working capital of 20% of the anticipated sales revenue for the year. Any remaining working capital will be released at the end of the project.

(vii) Working capital and depreciation have not been taken into account in the net present value calculation above, since depreciation is not a cash flow and all the working capital is returned at the end of the project.

It is anticipated that the project will be financed entirely by debt, 60% of which will be obtained from a subsidised loan scheme run by the government, which lends money at a rate of 100 basis points below the 10-year government debt yield rate of 2·5%. Issue costs related to raising the finance are 2% of the gross finance required. The remaining 40% will be funded from Burung Co’s normal borrowing sources. It can be assumed that the debt capacity available to Burung Co is equal to the actual amount of debt finance raised for the project.

Burung Co has identified a company, Lintu Co, which operates in the same line of business as that of the project it is considering. Lintu Co is financed by 40 million shares trading at $3·20 each and $34 million debt trading at $94 per $100. Lintu Co’s equity beta is estimated at 1·5. The current yield on government treasury bills is 2% and it is estimated that the market risk premium is 8%. Lintu Co pays tax at an annual rate of 20%.

Both Burung Co and Lintu Co pay tax in the same year as when profits are earned.

Required:

(a) Calculate the adjusted present value (APV) for the project, correcting any errors made in the net present value estimate above, and conclude whether the project should be accepted or not. Show all relevant calculations. (15 marks)

(b) Comment on the corrections made to the original net present value estimate and explain the APV approach taken in part (a), including any assumptions made. (10 marks)

第4题

Certified Accountants. You are currently reviewing the audit working papers for Pulp Co, a long standing audit client,

for the year ended 31 January 2008. The draft statement of financial position (balance sheet) of Pulp Co shows total

assets of $12 million (2007 – $11·5 million).The audit senior has made the following comment in a summary of

issues for your review:

‘Pulp Co’s statement of financial position (balance sheet) shows a receivable classified as a current asset with a value

of $25,000. The only audit evidence we have requested and obtained is a management representation stating the

following:

(1) that the amount is owed to Pulp Co from Jarvis Co,

(2) that Jarvis Co is controlled by Pulp Co’s chairman, Peter Sheffield, and

(3) that the balance is likely to be received six months after Pulp Co’s year end.

The receivable was also outstanding at the last year end when an identical management representation was provided,

and our working papers noted that because the balance was immaterial no further work was considered necessary.

No disclosure has been made in the financial statements regarding the balance. Jarvis Co is not audited by our firm

and we have verified that Pulp Co does not own any shares in Jarvis Co.’

Required:

(b) In relation to the receivable recognised on the statement of financial position (balance sheet) of Pulp Co as

at 31 January 2008:

(i) Comment on the matters you should consider. (5 marks)

第5题

responsible for reviewing invoices raised to clients and for monitoring your firm’s credit control procedures. Several

matters came to light during your most recent review of client invoice files:

Norman Co, a large private company, has not paid an invoice from Smith & Co dated 5 June 2007 for work in respect

of the financial statement audit for the year ended 28 February 2007. A file note dated 30 November 2007 states

that Norman Co is suffering poor cash flows and is unable to pay the balance. This is the only piece of information

in the file you are reviewing relating to the invoice. You are aware that the final audit work for the year ended

28 February 2008, which has not yet been invoiced, is nearly complete and the audit report is due to be issued

imminently.

Wallace Co, a private company whose business is the manufacture of industrial machinery, has paid all invoices

relating to the recently completed audit planning for the year ended 31 May 2008. However, in the invoice file you

notice an invoice received by your firm from Wallace Co. The invoice is addressed to Valerie Hobson, the manager

responsible for the audit of Wallace Co. The invoice relates to the rental of an area in Wallace Co’s empty warehouse,

with the following comment handwritten on the invoice: ‘rental space being used for storage of Ms Hobson’s

speedboat for six months – she is our auditor, so only charge a nominal sum of $100’. When asked about the invoice,

Valerie Hobson said that the invoice should have been sent to her private address. You are aware that Wallace Co

sometimes uses the empty warehouse for rental income, though this is not the main trading income of the company.

In the ‘miscellaneous invoices raised’ file, an invoice dated last week has been raised to Software Supply Co, not a

client of your firm. The comment box on the invoice contains the note ‘referral fee for recommending Software Supply

Co to several audit clients regarding the supply of bespoke accounting software’.

Required:

Identify and discuss the ethical and other professional issues raised by the invoice file review, and recommend

what action, if any, Smith & Co should now take in respect of:

(a) Norman Co; (8 marks)

第6题

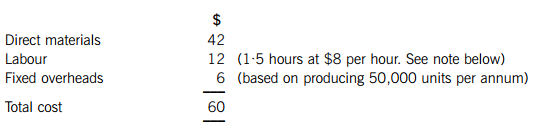

Heat Co is now trying to ascertain the best pricing policy that they should adopt for the Energy Buster’s launch onto the market. Demand is very responsive to price changes and research has established that, for every $15 increase in price, demand would be expected to fall by 1,000 units. If the company set the price at $735, only 1,000 units would be demanded.

The costs of producing each air conditioning unit are as follows:

Note

The first air conditioning unit took 1·5 hours to make and labour cost $8 per hour. A 95% learning curve exists, in relation to production of the unit, although the learning curve is expected to finish after making 100 units. Heat Co’s management have said that any pricing decisions about the Energy Buster should be based on the time it takes to make the 100th unit of the product. You have been told that the learning co-efficient, b = –0·0740005.

All other costs are expected to remain the same up to the maximum demand levels.

Required:

(a) (i) Establish the demand function (equation) for air conditioning units; (3 marks)

(ii) Calculate the marginal cost for each air conditioning unit after adjusting the labour cost as required by the note above; (6 marks)

(iii) Equate marginal cost and marginal revenue in order to calculate the optimum price and quantity. (3 marks)

(b) Explain what is meant by a ‘penetration pricing’ strategy and a ‘market skimming’ strategy and discuss whether either strategy might be suitable for Heat Co when launching the Energy Buster. (8 marks)

第7题

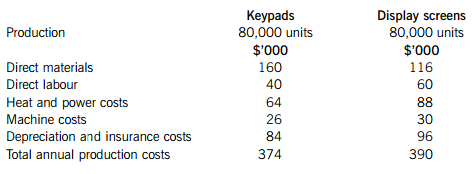

It currently produces and sells 80,000 units per annum, with production of them being restricted by the short supply of labour. Each control panel includes two main components – one key pad and one display screen. At present, Robber Co manufactures both of these components in-house. However, the company is currently considering outsourcing the production of keypads and/or display screens. A newly established company based in Burgistan is keen to secure a place in the market, and has offered to supply the keypads for the equivalent of $4·10 per unit and the display screens for the equivalent of $4·30 per unit. This price has been guaranteed for two years.

The current total annual costs of producing the keypads and the display screens are:

Notes:

1. Materials costs for keypads are expected to increase by 5% in six months’ time; materials costs for display screens are only expected to increase by 2%, but with immediate effect.

2. Direct labour costs are purely variable and not expected to change over the next year.

3. Heat and power costs include an apportionment of the general factory overhead for heat and power as well as the costs of heat and power directly used for the production of keypads and display screens. The general apportionment included is calculated using 50% of the direct labour cost for each component and would be incurred irrespective of whether the components are manufactured in-house or not.

4. Machine costs are semi-variable; the variable element relates to set up costs, which are based upon the number of batches made. The keypads’ machine has fixed costs of $4,000 per annum and the display screens’ machine has fixed costs of $6,000 per annum. Whilst both components are currently made in batches of 500, this would need to change, with immediate effect, to batches of 400.

5. 60% of depreciation and insurance costs relate to an apportionment of the general factory depreciation and insurance costs; the remaining 40% is specific to the manufacture of keypads and display screens.

Required:

(a) Advise Robber Co whether it should continue to manufacture the keypads and display screens in-house or whether it should outsource their manufacture to the supplier in Burgistan, assuming it continues to adopt a policy to limit manufacture and sales to 80,000 control panels in the coming year. (8 marks)

(b) Robber Co takes 0·5 labour hours to produce a keypad and 0·75 labour hours to produce a display screen. Labour hours are restricted to 100,000 hours and labour is paid at $1 per hour. Robber Co wishes to increase its supply to 100,000 control panels (i.e. 100,000 each of keypads and display screens). Advise Robber Co as to how many units of keypads and display panels they should either manufacture and/or outsource in order to minimise their costs. (7 marks)

(c) Discuss the non-financial factors that Robber Co should consider when making a decision about outsourcing the manufacture of keypads and display screens. (5 marks)

第8题

year end for each client is 30 September 2007.

You are reviewing the audit senior’s proposed audit reports for two clients, Alpha Co and Deema Co.

Alpha Co, a listed company, permanently closed several factories in May 2007, with all costs of closure finalised and

paid in August 2007. The factories all produced the same item, which contributed 10% of Alpha Co’s total revenue

for the year ended 30 September 2007 (2006 – 23%). The closure has been discussed accurately and fully in the

chairman’s statement and Directors’ Report. However, the closure is not mentioned in the notes to the financial

statements, nor separately disclosed on the financial statements.

The audit senior has proposed an unmodified audit opinion for Alpha Co as the matter has been fully addressed in

the chairman’s statement and Directors’ Report.

In October 2007 a legal claim was filed against Deema Co, a retailer of toys. The claim is from a customer who slipped

on a greasy step outside one of the retail outlets. The matter has been fully disclosed as a material contingent liability

in the notes to the financial statements, and audit working papers provide sufficient evidence that no provision is

necessary as Deema Co’s lawyers have stated in writing that the likelihood of the claim succeeding is only possible.

The amount of the claim is fixed and is adequately covered by cash resources.

The audit senior proposes that the audit opinion for Deema Co should not be qualified, but that an emphasis of matter

paragraph should be included after the audit opinion to highlight the situation.

Hugh Co was incorporated in October 2006, using a bank loan for finance. Revenue for the first year of trading is

$750,000, and there are hopes of rapid growth in the next few years. The business retails luxury hand made wooden

toys, currently in a single retail outlet. The two directors (who also own all of the shares in Hugh Co) are aware that

due to the small size of the company, the financial statements do not have to be subject to annual external audit, but

they are unsure whether there would be any benefit in a voluntary audit of the first year financial statements. The

directors are also aware that a review of the financial statements could be performed as an alternative to a full audit.

Hugh Co currently employs a part-time, part-qualified accountant, Monty Parkes, who has prepared a year end

balance sheet and income statement, and who produces summary management accounts every three months.

Required:

(a) Evaluate whether the audit senior’s proposed audit report is appropriate, and where you disagree with the

proposed report, recommend the amendment necessary to the audit report of:

(i) Alpha Co; (6 marks)

第9题

The following scenario relates to questions 11–15.

Mighty IT Co provides hardware, software and IT services to small business customers.

Mighty IT Co has developed an accounting software package. The company offers a supply and installation service for $1,000 and a separate two-year technical support service for $500. Alternatively, it also offers a combined goods and services contract which includes both of these elements for $1,200. Payment for the combined contract is due one month after the date of installation.

In December 20X5, Mighty IT Co revalued its corporate headquarters. Prior to the revaluation, the carrying amount of the building was $2m and it was revalued to $2·5m.

Mighty IT Co also revalued a sales office on the same date. The office had been purchased for $500,000 earlier in the year, but subsequent discovery of defects reduced its value to $400,000. No depreciation had been charged on the sales office and any impairment loss is allowable for tax purposes.

Mighty It Co’s income tax rate is 30%.

In accordance with IFRS 15 Revenue from Contracts with Customers, when should Mighty IT Co recognise revenue from the combined goods and services contract?

A.Supply and install: on installation Technical support: over two years

B.Supply and install: when payment is made Technical support: over two years

C.Supply and install: on installation Technical support: on installation

D.Supply and install: when payment is made Technical support: when payment is made

In January 20X6, the accountant at Mighty IT Co produced the company’s draft financial statements for the year ended 31 December 20X5. He then realised that he had omitted to consider deferred tax on development costs. In 20X5, development costs of $200,000 had been incurred and capitalised. Development costs are deductible in full for tax purposes in the year they are incurred. The development is still in process at 31 December 20X5.

What adjustment is required to the income tax expense in Mighty IT Co’s statement of profit or loss for the year ended 31 December 20X5 to account for deferred tax on the development costs?

A.Increase of $200,000

B.Increase of $60,000

C.Decrease of $60,000

D.Decrease of $200,000

For each combined contract sold, what is the amount of revenue which Mighty IT Co should recognise in respect of the supply and installation service in accordance with IFRS 15?A.$700

B.$800

C.$1,000

D.$1,200

In accordance with IAS 12 Income Taxes, what is the impact of the property revaluations on the income tax expense of Mighty IT Co for the year ended 31 December 20X5?

A.Income tax expense increases by $180,000

B.Income tax expense increases by $120,000

C.Income tax expense decreases by $30,000

D.No impact on income tax expense

Mighty IT Co sells a combined contract on 1 January 20X6, the first day of its financial year.

In accordance with IFRS 15, what is the total amount for deferred income which will be reported in Mighty IT Co’s statement of financial position as at 31 December 20X6?

A.$400

B.$250

C.$313

D.$200

请帮忙给出每个问题的正确答案和分析,谢谢!

第10题

Your company has an Active Directory Domain Servic es (AD DS) domain. All servers run Windows Server 2008 R2. All client computers run Windows 7. Your environment includes Microsoft Application Virtualization (App - V), Microsoft Enterprise Desktop Virtualization (MED - V), and Remote Desktop Services.You hav e three applications that are in one package and require authorization to run.You need to deploy the applications for offline use.What should you do?()

A.Configure a MED - V revertible workspace policy.

B.Configure the Remote Desktop Connection Broker (RD Co nnection Broker). Create a Group Policy object (GPO) to configure the Configure server authentication for client setting.

C.Use Microsoft Application Virtualization for Desktops. On each client computer, set the client cache configuration settings to Use f ree disk space threshold and configure the ApplicationSourceRoot registry key.

D.Use Microsoft Application Virtualization for Desktops. On each client computer, configure the AutoLoad Triggers, AutoLoadTarget andRequireAuthorizationIfCached registry paramet ers. Then launch any one of the applications while logged in with the computer user is credentials.

第11题

The audit work for the year ended 30 June 2015 is nearly complete, and you are reviewing the draft audit report which has been prepared by the audit senior. During the year the Hopper Group purchased a new subsidiary company, Seurat Sweeteners Co, which has expertise in the research and design of sugar alternatives. The draft financial statements of the Hopper Group for the year ended 30 June 2015 recognise profit before tax of $495 million (2014 – $462 million) and total assets of $4,617 million (2014: $4,751 million). An extract from the draft audit report is shown below:

Basis of modified opinion (extract)

In their calculation of goodwill on the acquisition of the new subsidiary, the directors have failed to recognise consideration which is contingent upon meeting certain development targets. The directors believe that it is unlikely that these targets will be met by the subsidiary company and, therefore, have not recorded the contingent consideration in the cost of the acquisition. They have disclosed this contingent liability fully in the notes to the financial statements. We do not feel that the directors’ treatment of the contingent consideration is correct and, therefore, do not believe that the criteria of the relevant standard have been met. If this is the case, it would be appropriate to adjust the goodwill balance in the statement of financial position.

We believe that any required adjustment may materially affect the goodwill balance in the statement of financial position. Therefore, in our opinion, the financial statements do not give a true and fair view of the financial position of the Hopper Group and of the Hopper Group’s financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards.

Emphasis of Matter Paragraph

We draw attention to the note to the financial statements which describes the uncertainty relating to the contingent consideration described above. The note provides further information necessary to understand the potential implications of the contingency.

Required:

(a) Critically appraise the draft audit report of the Hopper Group for the year ended 30 June 2015, prepared by the audit senior.

Note: You are NOT required to re-draft the extracts from the audit report. (10 marks)

(b) The audit of the new subsidiary, Seurat Sweeteners Co, was performed by a different firm of auditors, Fish Associates. During your review of the communication from Fish Associates, you note that they were unable to obtain sufficient appropriate evidence with regard to the breakdown of research expenses. The total of research costs expensed by Seurat Sweeteners Co during the year was $1·2 million. Fish Associates has issued a qualified audit opinion on the financial statements of Seurat Sweeteners Co due to this inability to obtain sufficient appropriate evidence.

Required:

Comment on the actions which Rockwell & Co should take as the auditor of the Hopper Group, and the implications for the auditor’s report on the Hopper Group financial statements. (6 marks)

(c) Discuss the quality control procedures which should be carried out by Rockwell & Co prior to the audit report on the Hopper Group being issued. (4 marks)

相关内容

相关内容

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!