重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

The director required that every member in his department ______ to his report.

A.refer B.referred C.has referred D.refers

更多“The director required that every member in his department ______ to his report. A.refer B.referred”相关的问题

更多“The director required that every member in his department ______ to his report. A.refer B.referred”相关的问题

第1题

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

第2题

from larger competitors in their core food and drink markets. They are also finding it hard to respond to these

competitors moving into the sale of clothing and household goods. Supaserve has a reputation for friendly customer

care and is looking at the feasibility of introducing an online shopping service, from which customers can order goods

from the comfort of their home and have them delivered, for a small charge, to their home.

Chris recognises that the move to develop an online shopping service will require significant investment in new

technology and support systems. He hopes a significant proportion of existing and most importantly, new customers,

will be attracted to the new service.

Required:

(a) What bases for segmenting this new market would you recommend and what criteria will help determine

whether this segment is sufficiently attractive to commit to the necessary investment? (10 marks)

第3题

(a) Contrast the role of internal and external auditors. (8 marks)

(b) Conoy Co designs and manufactures luxury motor vehicles. The company employs 2,500 staff and consistently makes a net profit of between 10% and 15% of sales. Conoy Co is not listed; its shares are held by 15 individuals, most of them from the same family. The maximum shareholding is 15% of the share capital.

The executive directors are drawn mainly from the shareholders. There are no non-executive directors because the company legislation in Conoy Co’s jurisdiction does not require any. The executive directors are very successful in running Conoy Co, partly from their training in production and management techniques, and partly from their ‘hands-on’ approach providing motivation to employees.

The board are considering a significant expansion of the company. However, the company’s bankers are

concerned with the standard of financial reporting as the financial director (FD) has recently left Conoy Co. The board are delaying provision of additional financial information until a new FD is appointed.

Conoy Co does have an internal audit department, although the chief internal auditor frequently comments that the board of Conoy Co do not understand his reports or provide sufficient support for his department or the internal control systems within Conoy Co. The board of Conoy Co concur with this view. Anders & Co, the external auditors have also expressed concern in this area and the fact that the internal audit department focuses work on control systems, not financial reporting. Anders & Co are appointed by and report to the board of Conoy Co.

The board of Conoy Co are considering a proposal from the chief internal auditor to establish an audit committee.

The committee would consist of one executive director, the chief internal auditor as well as three new appointees.

One appointee would have a non-executive seat on the board of directors.

Required:

Discuss the benefits to Conoy Co of forming an audit committee. (12 marks)

第4题

1 The scientists in the research laboratories of Swan Hill Company (SHC, a public listed company) recently made a very

important discovery about the process that manufactured its major product. The scientific director, Dr Sonja Rainbow,

informed the board that the breakthrough was called the ‘sink method’. She explained that the sink method would

enable SHC to produce its major product at a lower unit cost and in much higher volumes than the current process.

It would also produce lower unit environmental emissions and would substantially improve product quality compared

to its current process and indeed compared to all of the other competitors in the industry.

SHC currently has 30% of the global market with its nearest competitor having 25% and the other twelve producers

sharing the remainder. The company, based in the town of Swan Hill, has a paternalistic management approach and

has always valued its relationship with the local community. Its website says that SHC has always sought to maximise

the benefit to the workforce and community in all of its business decisions and feels a great sense of loyalty to the

Swan Hill locality which is where it started in 1900 and has been based ever since.

As the board considered the implications of the discovery of the sink method, chief executive Nelson Cobar asked

whether Sonja Rainbow was certain that SHC was the only company in the industry that had made the discovery and

she said that she was. She also said that she was certain that the competitors were ‘some years’ behind SHC in their

research.

It quickly became clear that the discovery of the sink method was so important and far reaching that it had the

potential to give SHC an unassailable competitive advantage in its industry. Chief executive Nelson Cobar told board

colleagues that they should clearly understand that the discovery had the potential to put all of SHC’s competitors out

of business and make SHC the single global supplier. He said that as the board considered the options, members

should bear in mind the seriousness of the implications upon the rest of the industry.

Mr Cobar said there were two strategic options. Option one was to press ahead with the huge investment of new plant

necessary to introduce the sink method into the factory whilst, as far as possible, keeping the nature of the sink

technology secret from competitors (the ‘secrecy option’). A patent disclosing the nature of the technology would not

be filed so as to keep the technology secret within SHC. Option two was to file a patent and then offer the use of the

discovery to competitors under a licensing arrangement where SHC would receive substantial royalties for the twentyyear

legal lifetime of the patent (the ‘licensing option’). This would also involve new investment but at a slower pace

in line with competitors. The licence contract would, Mr Cobar explained, include an ‘improvement sharing’

requirement where licensees would be required to inform. SHC of any improvements discovered that made the sink

method more efficient or effective.

The sales director, Edwin Kiama, argued strongly in favour of the secrecy option. He said that the board owed it to

SHC’s shareholders to take the option that would maximise shareholder value. He argued that business strategy was

all about gaining competitive advantage and this was a chance to do exactly that. Accordingly, he argued, the sink

method should not be licensed to competitors and should be pursued as fast as possible. The operations director said

that to gain the full benefits of the sink method with either option would require a complete refitting of the factory and

the largest capital investment that SHC had ever undertaken.

The financial director, Sean Nyngan, advised the board that pressing ahead with investment under the secrecy option

was not without risks. First, he said, he would have to finance the investment, probably initially through debt, and

second, there were risks associated with any large investment. He also informed the board that the licensing option

would, over many years, involve the inflow of ‘massive’ funds in royalty payments from competitors using the SHC’s

patented sink method. By pursuing the licensing option, Sean Nyngan said that they could retain their market

leadership in the short term without incurring risk, whilst increasing their industry dominance in the future through

careful investment of the royalty payments.

The non-executive chairman, Alison Manilla, said that she was looking at the issue from an ethical perspective. She

asked whether SHC had the right, even if it had the ability, to put competitors out of business.

Required:

(a) Assess the secrecy option using Tucker’s model for decision-making. (10 marks)

第5题

palaces, temples, houses and factories) which attract visitors from home and abroad. Most of these tourist sites have

gift shops where visitors can buy mementos and souvenirs of their visit. These souvenirs often include cups, saucers,

plates and other items which feature a printed image of the particular tourist site.

The Universal Pottery Company (UPC) is the main supplier of these pottery souvenir items to the tourist trade. It

produces the items in its potteries and then applies the appropriate image using specialised image printing machines.

UPC also supplies other organisations that require personalised products. For example, it recently won the right to

produce souvenirs for the Eurasian Games, which are being held in Europia in two years time. UPC currently ships

about 250,000 items of pottery out of its factory every month. Most of these items are shipped in relatively small

packages. All collections from the factory and deliveries to customers are made by a nationwide courier company.

In the last two years there has been a noticeable increase in the number of complaints about the quality of these

items. The complaints, from gift shop owners, concentrate on two main issues:

(i) The physical condition of goods when they arrive at the gift shop. Initial evidence suggests that ‘a significant

number of products are now arriving broken, chipped or cracked’. These items are unusable and they have to be

returned to UPC. UPC management are convinced that the increased breakages are due to packers not following

the correct packing method.

(ii) Incorrect alignment of the image of the tourist site on the selected item. For example, a recent batch of 100 cups

for Carish Castle included 10 cups where the image of the castle sloped significantly from left to right. These

were returned by the customer and destroyed by UPC.

The image problem was investigated in more depth and it was discovered that approximately 500 items were

delivered every month with misaligned images. Each item costs, on average, $20 to produce.

As a result of these complaints, UPC appointed a small quality inspection team who were asked to inspect one in

every 20 packages for correct packaging and correct image alignment. However, although some problems have been

found, a significant number of defective products have still been delivered to customers. A director of UPC used this

evidence to support his assertion that the ‘quality inspection team is just not working’.

The payment system for packers has also been such an issue. It was established ten years ago as an attempt to boost

productivity. Packers receive a bonus for packing more than a target number of packages per hour. Hence, packers

are more concerned with the speed of packing rather than its quality.

Finally, there is also evidence that to achieve agreed customer deadlines, certain managers have asked the quality

inspection team to overlook defective items so that order deadlines could be met.

The company has decided to review the quality issue again. The director who claimed that the quality inspection team

is not working has suggested using a Six Sigma approach to the company’s quality problems.

Required:

(a) Analyse the current and potential role of quality, quality control and quality assurance at UPC. (15 marks)

第6题

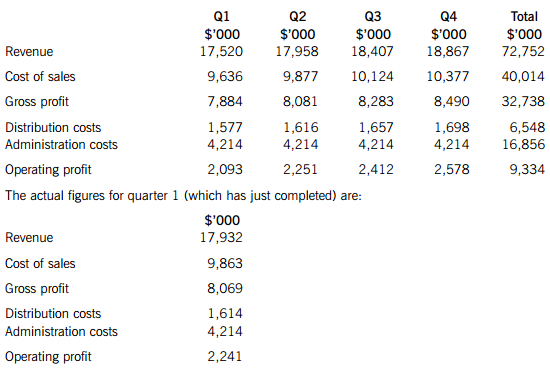

The Drinks Group (DG) has been created over the last three years by merging three medium-sized family businesses. These businesses are all involved in making fruit drinks. Fizzy (F) makes and bottles healthy, fruit-based sparkling drinks. Still (S) makes and bottles fruit-flavoured non-sparkling drinks and Healthy (H) buys fruit and squeezes it to make basic fruit juices. The three companies have been divisionalised within the group structure. A fourth division called Marketing (M) exists to market the products of the other divisions to various large retail chains. Marketing has only recently been set up in order to help the business expand. All of the operations and sales of DG occur in Nordland, which is an economically well-developed country with a strong market for healthy non-alcoholic drinks.

—————————————————————————————————————————

The group has recruited a new finance director (FD), who was asked by the board to perform. a review of the efficiency and effectiveness of the finance department as her first task on taking office. The finance director has just presented her report to the board regarding some problems at DG.

Extract from finance director’s Report to the Board:

‘The main area for improvement, which was discussed at the last board meeting, is the need to improve profit margins throughout the business. There is no strong evidence that new products or markets are required but that the most promising area for improvement lies in better internal control practices.

Control

As DG was formed from an integration of the original businesses (F, S, H), there was little immediate effort put into optimising the control systems of these businesses. They have each evolved over time in their own way. Currently, the main method of central control that can be used to drive profit margin improvement is the budget system in each business. The budgeting method used is to take the previous year’s figures and simply increment them by estimates of growth in the market that will occur over the next year. These growth estimates are obtained through a discussion between the financial managers at group level and the relevant divisional managers. The management at each division are then given these budgets by head office and their personal targets are set around achieving the relevant budget numbers.

Divisions

H and S divisions are in stable markets where the levels of demand and competition mean that sales growth is unlikely, unless by acquisition of another brand. The main engine for prospective profit growth in these divisions is through margin improvements. The managers at these divisions have been successful in previous years and generally keep to the agreed budgets. As a result, they are usually not comfortable with changing existing practices.

F is faster growing and seen as the star of the Group. However, the Group has been receiving complaints from customers about late deliveries and poor quality control of the F products. The F managers have explained that they are working hard within the budget and capital constraints imposed by the board and have expressed a desire to be less controlled.

The marketing division has only recently been set up and the intention is to run each marketing campaign as an individual project which would be charged to the division whose products are benefiting from the campaign. The managers of the manufacturing divisions are very doubtful of the value of M, as each believes that they have an existing strong reputation with their customers that does not require much additional spending on marketing. However, the board decided at the last meeting that there was scope to create and use a marketing budget effectively at DG, if its costs were carefully controlled. Similar to the other divisions, the marketing division budgets are set by taking the previous year’s actual spend and adding a percentage increase. For M, the increase corresponds to the previous year’s growth in group turnover.’

End of extract

—————————————————————————————————————————

At present, the finance director is harassed by the introduction of a new information system within the finance department which is straining the resources of the department. However, she needs to respond to the issues raised above at the board meeting and so is considering using different budgeting methods at DG. She has asked you, the management accountant at the Group, to do some preliminary work to help her decide whether and how to change the budget methods. The first task that she believes would be useful is to consider the use of rolling budgets. She thinks that fast-growing F may prove the easiest division in which to introduce new ideas.

F’s incremental budget for the current year is given below. You can assume that cost of sales and distribution costs are variable and administrative costs are fixed.

On the basis of the Q1 results, sales volume growth of 3% per quarter is now expected.

The finance director has also heard you talking about bottom-up budgeting and wants you to evaluate its use at DG.

Required:

(a) Evaluate the suitability of incremental budgeting at each division. (8 marks)

(b) Recalculate the budget for Fizzy division (F) using rolling budgeting and assess the use of rolling budgeting at F. (8 marks)

(c) Recommend any appropriate changes to the budgeting method at the Marketing division (M), providing justifications for your choice. (4 marks)

(d) Analyse and recommend the appropriate level of participation in budgeting at Drinks Group (DG). (6 marks)

第7题

The future health of Americans may depend on it. Just this week, a study reported that life expectancy (预期寿命) has fallen or is no longer increasing in some parts of the United States. The situation is worst among poor people in the southern states, and especially women. Public health researchers say it is largely the result of increases in obesity (肥胖), smoking and high blood pressure. They also blame differences in health services around the country.

In 2006, a study found that only four percent of elementary schools provided daily physical education all year for all grades. This was true of eight percent of middle schools and two percent of high schools. The study also found that 22 percent of all schools did not require students to take any P. E. (体育课).

Charlene Burgeson is the executive director of the National Association for Sport and Physical Education. She says one problem for P. E. teachers is that schools are under pressure to put more time into academic subjects. Also, parents may agree that children need exercise in school. Yet many parents today still have bad memories of being chosen last for teams because teachers favored the good athletes in class.

But experts say P. E. classes have changed. They say the goal has moved away from competition and toward personal performance, as a way tp build a lifetime of activity. These days, teachers often lead activities like weight training and yoga. Some parents like the idea of avoiding competitive sports in P.E class. Yet others surely dislike that idea. In the end, schools may find themselves in a no-win situation.

Why are schools recommended to give students certain time for sports?

A.Because different schools set up different physical education programs.

B.Because the physical activity of children will influence their health in adulthood.

C.Because nowadays children spend too much time on their studies.

D.Because only four percent of elementary schools provided daily physical education.

第8题

£32,000 and is provided with a petrol-driven company car which has a CO2 emission rate of 187g/km and had a

list price when new of £22,360. In August 2003, when he was first provided with the car, Benny paid the company

£6,100 towards the capital cost of the car. Golden Tan plc does not pay for any of Benny’s private petrol and he is

also required to pay his employer £18 per month as a condition of being able to use the car for private purposes.

On 1 December 2006 Golden Tan plc notified Benny that he would be made redundant on 28 February 2007. On

that day the company will pay him his final month’s salary together with a payment of £8,000 in lieu of the three

remaining months of his six-month notice period in accordance with his employment contract. In addition the

company will pay him £17,500 in return for agreeing not to work for any of its competitors for the six-month period

ending 31 August 2007.

On receiving notification of his redundancy, Benny immediately contacted Joe Egmont, the managing director of

Summer Glow plc, who offered him a senior management position leading the company’s expansion into Eastern

Europe. Summer Glow plc is one of Golden Tan plc’s competitors and one of the most innovative companies in the

industry, although not all of its strategies have been successful.

Benny has agreed to join Summer Glow plc on 1 September 2007 for an annual salary of £39,000. On the day he

joins the company, Summer Glow plc will grant him an option to purchase 10,000 ordinary shares in the company

for £2·20 per share under an unapproved share option scheme. Benny can exercise the option once he has been

employed for six months but must hold the shares for at least a year before he sells them.

The new job will require Benny to spend a considerable amount of time in London. Summer Glow plc has offered

Benny the exclusive use of a flat that the company purchased on 1 June 2003 for £165,000; the flat is currently

rented out. The flat will be made available from 1 September 2007. The company will pay all of the utility bills

relating to the flat as well as furnishing and maintaining it. Summer Glow plc has also suggested that if Benny would

rather live in a more central part of the city, the company could sell the existing flat and buy a more centrally located

one, of the same value, with the proceeds.

On 15 March 2007 Benny intends to sell 5,800 shares in Mahana plc, a quoted company, for £24,608. His

transactions in the company’s shares have been as follows:

£

June 1988 Purchased 8,400 shares 6,744

February 1996 Sale of rights nil paid 610

January 2005 Purchased 1,300 shares 2,281

The sale of rights, nil paid, was not treated as a part disposal of Benny’s holding in Mahana plc.

Benny’s shareholding in Mahana plc represents less than 1% of the company’s issued ordinary share capital. He will

not make any other capital disposals in 2006/07.

In addition to his employment income, Benny receives rental income of £4,000 (net of deductible expenses) each

year. He normally submits his tax return in August but he has not yet prepared his return for 2005/06. He expects

to be very busy in December and January and is planning to prepare his tax return in late February 2007.

Required:

(a) Calculate Benny’s employment income for 2006/07. (4 marks)

第9题

The director was critical ______ the way we were doing the work.

A) atB) inC)ofD) with

第10题

A.SELECT * FROM Movie WHERE director LIKE ‘_a_’;

B.SELECT * FROM Movie WHERE director LIKE ‘%a%’;

C.SELECT * FROM Movie WHERE director LIKE ‘%a_’;

D.SELECT * FROM Movie WHERE director LIKE ‘_a%’;

相关内容

相关内容

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!