重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

A. $10,000.

B. $13,340.

C. $14,200.

更多“A company leased equipment under a seven-year finance lease requiring year-end payment”相关的问题

更多“A company leased equipment under a seven-year finance lease requiring year-end payment”相关的问题

第1题

A.wishes to show a higher cash flow from operations.

B.desires a lower debt-to-equity ratio.

C.has a low marginal tax rate.

第2题

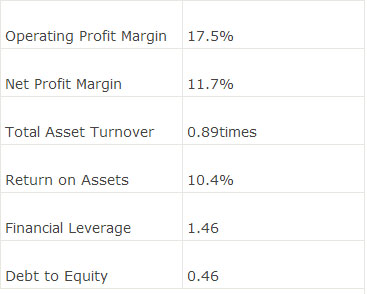

An analyst has calculated the following ratios for a company:

The company’s return on equity (ROE) is closestto:

A.4.8%.

B.15.2%.

C.22.7%.

第3题

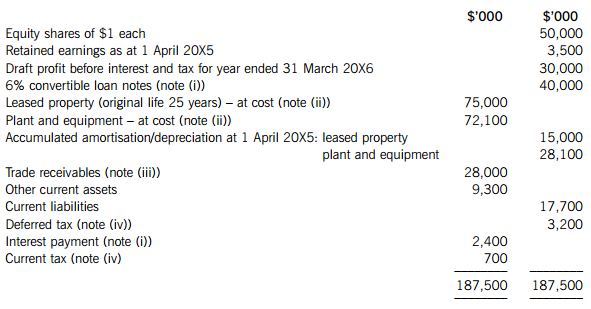

After preparing a draft statement of profit or loss (before interest and tax) for the year ended 31 March 20X6 (before any adjustments which may be required by notes (i) to (iv) below), the summarised trial balance of Triage Co as at 31 March 20X6 is:

The following notes are relevant:

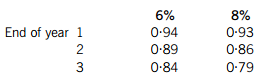

(i) Triage Co issued 400,000 $100 6% convertible loan notes on 1 April 20X5. Interest is payable annually in arrears on 31 March each year. The loans can be converted to equity shares on the basis of 20 shares for each $100 loan note on 31 March 20X8 or redeemed at par for cash on the same date. An equivalent loan without the conversion rights would have required an interest rate of 8%.

The present value of $1 receivable at the end of each year, based on discount rates of 6% and 8%, are:

(ii) Non-current assets:

The directors decided to revalue the leased property at $66·3m on 1 October 20X5. Triage Co does not make an annual transfer from the revaluation surplus to retained earnings to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability at the company’s tax rate of 20%.

The leased property is depreciated on a straight-line basis and plant and equipment at 15% per annum using the reducing balance method.

No depreciation has yet been charged on any non-current assets for the year ended 31 March 20X6.

(iii) In September 20X5, the directors of Triage Co discovered a fraud. In total, $700,000 which had been included as receivables in the above trial balance had been stolen by an employee. $450,000 of this related to the year ended 31 March 20X5, the rest to the current year. The directors are hopeful that 50% of the losses can be recovered from the company’s insurers.

(iv) A provision of $2·7m is required for current income tax on the profit of the year to 31 March 20X6. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (ii), at 31 March 20X6, the carrying amounts of Triage Co’s net assets are $12m more than their tax base.

Required:

(a) Prepare a schedule of adjustments required to the draft profit before interest and tax (in the above trial balance) to give the profit or loss of Triage Co for the year ended 31 March 20X6 as a result of the information in notes (i) to (iv) above.

(b) Prepare the statement of financial position of Triage Co as at 31 March 20X6.

(c) The issue of convertible loan notes can potentially dilute the basic earnings per share (EPS). Calculate the diluted earnings per share for Triage Co for the year ended 31 March 20X6 (there is no need to calculate the basic EPS).

Note: A statement of changes in equity and the notes to the statement of financial position are not required.

The following mark allocation is provided as guidance for this question:

(a) 5 marks

(b) 12 marks

(c) 3 marks

第4题

situations under IAS12 ‘Income Taxes’:

(i) On 1 November 2003, the company had granted ten million share options worth $40 million subject to a two

year vesting period. Local tax law allows a tax deduction at the exercise date of the intrinsic value of the options.

The intrinsic value of the ten million share options at 31 October 2004 was $16 million and at 31 October 2005

was $46 million. The increase in the share price in the year to 31 October 2005 could not be foreseen at

31 October 2004. The options were exercised at 31 October 2005. The directors are unsure how to account

for deferred taxation on this transaction for the years ended 31 October 2004 and 31 October 2005.

(ii) Panel is leasing plant under a finance lease over a five year period. The asset was recorded at the present value

of the minimum lease payments of $12 million at the inception of the lease which was 1 November 2004. The

asset is depreciated on a straight line basis over the five years and has no residual value. The annual lease

payments are $3 million payable in arrears on 31 October and the effective interest rate is 8% per annum. The

directors have not leased an asset under a finance lease before and are unsure as to its treatment for deferred

taxation. The company can claim a tax deduction for the annual rental payment as the finance lease does not

qualify for tax relief.

(iii) A wholly owned overseas subsidiary, Pins, a limited liability company, sold goods costing $7 million to Panel on

1 September 2005, and these goods had not been sold by Panel before the year end. Panel had paid $9 million

for these goods. The directors do not understand how this transaction should be dealt with in the financial

statements of the subsidiary and the group for taxation purposes. Pins pays tax locally at 30%.

(iv) Nails, a limited liability company, is a wholly owned subsidiary of Panel, and is a cash generating unit in its own

right. The value of the property, plant and equipment of Nails at 31 October 2005 was $6 million and purchased

goodwill was $1 million before any impairment loss. The company had no other assets or liabilities. An

impairment loss of $1·8 million had occurred at 31 October 2005. The tax base of the property, plant and

equipment of Nails was $4 million as at 31 October 2005. The directors wish to know how the impairment loss

will affect the deferred tax provision for the year. Impairment losses are not an allowable expense for taxation

purposes.

Assume a tax rate of 30%.

Required:

(b) Discuss, with suitable computations, how the situations (i) to (iv) above will impact on the accounting for

deferred tax under IAS12 ‘Income Taxes’ in the group financial statements of Panel. (16 marks)

(The situations in (i) to (iv) above carry equal marks)

第5题

A. A CSU/DSU converts analog signals from a router to a leased line; a modem converts analog signals from a router to a leased line.

B. A CSU/DSU converts analog signals from a router to a phone line; a modem converts digital signals from a router to a leased line.

C. A CSU/DSU converts digital signals from a router to a phone line; a modem converts analog signals from a router to a phone line.

D. A CSU/DSU converts digital signals from a router to a leased line; a modem converts digital signals from a router to a phone line.

第7题

A.bond

B.caveat emptor

C.warranty

D.collateral

第8题

A. IPsec tunnel

B. GRE tunnel

C. Floating stati c route

D. An IGP

第9题

A.They create split-horizon issues

B.They require a unique subnet within a routing domain

C.They emulate leased lines

D.They are ideal for full-mesh topologies

E.They require the use of NBMA options when using OSPF

第10题

A.network or subnetwork IP address

B.broadcast address on the network

C.IP address leased to the LAN

D.IP address used by the interfaces

E.manually assigned address to the clients

F.designated IP address to the DHCP server

相关内容

相关内容

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是()。

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“金降落伞”策略。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“焦土策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“白衣骑士”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“毒丸策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略不是()。

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是()。

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“金降落伞”策略。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“焦土策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“白衣骑士”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“毒丸策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略不是()。

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!