重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

(a) The following figures have been calculated from the financial statements (including comparatives) of Barstead for

the year ended 30 September 2009:

increase in profit after taxation 80%

increase in (basic) earnings per share 5%

increase in diluted earnings per share 2%

Required:

Explain why the three measures of earnings (profit) growth for the same company over the same period can

give apparently differing impressions. (4 marks)

(b) The profit after tax for Barstead for the year ended 30 September 2009 was $15 million. At 1 October 2008 the company had in issue 36 million equity shares and a $10 million 8% convertible loan note. The loan note will mature in 2010 and will be redeemed at par or converted to equity shares on the basis of 25 shares for each $100 of loan note at the loan-note holders’ option. On 1 January 2009 Barstead made a fully subscribed rights issue of one new share for every four shares held at a price of $2·80 each. The market price of the equity shares of Barstead immediately before the issue was $3·80. The earnings per share (EPS) reported for the year ended 30 September 2008 was 35 cents.

Barstead’s income tax rate is 25%.

Required:

Calculate the (basic) EPS figure for Barstead (including comparatives) and the diluted EPS (comparatives not required) that would be disclosed for the year ended 30 September 2009. (6 marks)

更多“(a) The following figures have been calculated from the financial statements (including co”相关的问题

更多“(a) The following figures have been calculated from the financial statements (including co”相关的问题

第1题

Which of the following is equivalent to a lump sum contract:

A fixed price contract

B price fixing contract

C purchase order

D All of the above.

E B and C only

第2题

Which of the following desdription is WRONG .about Wi-Fi? ().

A.Any standard Wi~Fi device. will work anywhere in the world with global operative set of standaeds

B.Now most laptops are built with wireless network adapters inside

C.One can connect Wi-Fi devices in ad-hoc mode for client-to-client connections without a router

D.Communications between two devices need the involvement of an access point with Wi-Fi

第3题

A、It is equal to the duration of the assets minus the duration of the liabilities.

B、Larger the gap in absolute terms, the more exposed the FI is to interest rate shocks.

C、It reflects the degree of maturity mismatch in an FI's balance sheet.

D、It indicates the dollar size of the potential net worth.

E、Its value is equal to duration divided by (1 + R).

第4题

132 Which of the following contract types has the highest risk to the contractor:

A. Firm fixed price (FFP)

B. Time and material (T&M)

C. Cost plus fixed fee (CPFF)

D. Cost plus incentive fee (CPIF)

E. A and B only

第5题

A.a living chicken

B.a dead chicken

C.historical evidence that there are only finitely many generations of any extant species

D.the combination of A and B,but not C

E.the combination of A and C,but not B

第6题

A、Periodic cash flow of interest and principal amortization payments on long-term assets that can be reinvested at market rates.

B、The effect that a change in the spread between rates on RSAs and RSLs has on net interest income as interest rates change.

C、Mismatch of asset and liabilities within a maturity bucket.

D、The relations between changes in interest rates and changes in net interest income.

E、Those deposits that act as an FI's long-term sources of funds.

第7题

A、Its information value is limited.

B、It accounts for the problem of rate-insensitive asset and liability runoffs and prepayments.

C、It accommodates cash flows from off-balance-sheet activities.

D、It helps to determine an FI's profit exposure to interest rate changes.

E、It considers market value effects of interest rate changes.

第8题

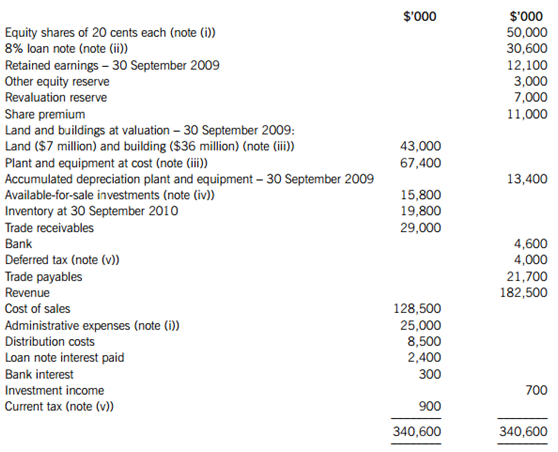

The following trial balance relates to Cavern as at 30 September 2010:

The following notes are relevant:

(i) Cavern has accounted for a fully subscribed rights issue of equity shares made on 1 April 2010 of one new share for every four in issue at 42 cents each. The company paid ordinary dividends of 3 cents per share on 30 November 2009 and 5 cents per share on 31 May 2010. The dividend payments are included in administrative expenses in the trial balance.

(ii) The 8% loan note was issued on 1 October 2008 at its nominal (face) value of $30 million. The loan note will be redeemed on 30 September 2012 at a premium which gives the loan note an effective fi nance cost of 10% per annum.

(iii) Non-current assets:

Cavern revalues its land and building at the end of each accounting year. At 30 September 2010 the relevant value to be incorporated into the fi nancial statements is $41·8 million. The building’s remaining life at the beginning of the current year (1 October 2009) was 18 years. Cavern does not make an annual transfer from the revaluation reserve to retained earnings in respect of the realisation of the revaluation surplus. Ignore deferred tax on the revaluation surplus.

Plant and equipment includes an item of plant bought for $10 million on 1 October 2009 that will have a 10-year life (using straight-line depreciation with no residual value). Production using this plant involves toxic chemicals which will cause decontamination costs to be incurred at the end of its life. The present value of these costs using a discount rate of 10% at 1 October 2009 was $4 million. Cavern has not provided any amount for this future decontamination cost. All other plant and equipment is depreciated at 12·5% per annum using the reducing balance method.

No depreciation has yet been charged on any non-current asset for the year ended 30 September 2010. All depreciation is charged to cost of sales.

(iv) The available-for-sale investments held at 30 September 2010 had a fair value of $13·5 million. There were no acquisitions or disposals of these investments during the year ended 30 September 2010.

(v) A provision for income tax for the year ended 30 September 2010 of $5·6 million is required. The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2009. At 30 September 2010 the tax base of Cavern’s net assets was $15 million less than their carrying amounts. The movement on deferred tax should be taken to the income statement. The income tax rate of Cavern is 25%.

Required:

(a) Prepare the statement of comprehensive income for Cavern for the year ended 30 September 2010.

(b) Prepare the statement of changes in equity for Cavern for the year ended 30 September 2010.

(c) Prepare the statement of fi nancial position of Cavern as at 30 September 2010.

Notes to the fi nancial statements are not required.

The following mark allocation is provided as guidance for this question:

(a) 11 marks

(b) 5 marks

(c) 9 marks

第9题

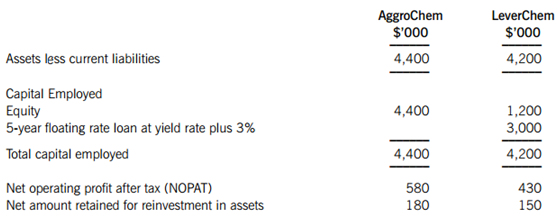

AggroChem is a fully listed company fi nanced wholly by equity. LeverChem is listed on an alternative investment market. Both companies have been trading for over 10 years and have shown strong levels of profi tability recently. However, both companies’ shares are thinly traded. It is thought that the current market value of LeverChem’s shares at higher than the book value is accurate, but it is felt that AggroChem shares are not quoted accurately by the market.

higher than the book value is accurate, but it is felt that AggroChem shares are not quoted accurately by the market.

The following information is taken from the fi nancial statements of both companies at the start of the current year:

It can be assumed that the retained earnings for both companies are equal to the net reinvestment in assets.

The assets of both companies are stated at fair value. Discussions with the AtReast Bank have led to an agreement that the fl oating rate loan to LeverChem can be transferred to the combined business on the same terms. The current yield rate is 5% and the current equity risk premium is 6%. It can be assumed that the risk free rate of return is equivalent to the yield rate. AggroChem’s beta has been estimated to be 1·26.

AggroChem Co wants to use the Black-Scholes option pricing (BSOP) model to assess the value of the combined business and the maximum premium payable to LeverChem’s shareholders. AggroChem has conducted a review of the volatility of the NOPAT values of both companies since both were formed and has estimated that the volatility of the combined business assets, if the acquisition were to go ahead, would be 35%. The exercise price should be calculated as the present value of a discount (zero-coupon) bond with an identical yield and term to maturity of the current bond.

Required:

Prepare a report for the management of AggroChem on the valuation of the combined business following acquisition and the maximum premium payable to the shareholders of LeverChem. Your report should:

(i) Using the free cash fl ow model, estimate the market value of equity for AggroChem Co, explaining any assumptions made. (9 marks)

(ii) Explain the circumstances in which the Black-Scholes option pricing (BSOP) model could be used to assess the value of a company, including the data required for the variables used in the model. (5 marks)

(iii) Using the BSOP methodology, estimate the maximum price and premium AggroChem may pay for LeverChem. (9 marks)

(iv) Discuss the appropriateness of the method used in part (iii) above, by considering whether the BSOP model can provide a meaningful value for a company. (5 marks)

Professional marks will be awarded in question 2 for the clarity and presentation of the report. (4 marks)

第11题

A、benefits the FI by increasing the market value of the FI's liabilities

B、harms the FI by increasing the market value of the FI's liabilities

C、harms the FI by decreasing the market value of the FI's liabilities

D、benefits the FI by decreasing the market value of the FI's liabilities

E、benefits the FI by decreasing the market value of the FI's assets

相关内容

相关内容

发站给中途站预留的包房,可利用其发售最远至预留站的车票()

执勤分队集体外出活动.除当班哨兵外.营区至少保留三班哨的兵力()

骑士小张送餐多了发现有时候顾客不方便出来当面接收货品,小张总结下来觉得送到门卫处/前台/门口等指定的位置后跟客户再三确认是否无误,还得用水印相机拍照通过APP“消息”发给顾客,这样就万无一失了,小张的做法对吗()

新员工入职,按照公司要求到指定医院体检产生的体检费用可自行报销,报销标准为100元/人,报销期限为其入职时间的3个月内()

XT5全系标配EPB电子驻车制动系统()

设备损坏引起水浸,由“谁管理,谁负责”实施,如属自来水公司负责,则由自来水公司负责抢修,物业公司提供协助;如属自管设备,自行组织力量抢修()

发站给中途站预留的包房,可利用其发售最远至预留站的车票()

执勤分队集体外出活动.除当班哨兵外.营区至少保留三班哨的兵力()

骑士小张送餐多了发现有时候顾客不方便出来当面接收货品,小张总结下来觉得送到门卫处/前台/门口等指定的位置后跟客户再三确认是否无误,还得用水印相机拍照通过APP“消息”发给顾客,这样就万无一失了,小张的做法对吗()

新员工入职,按照公司要求到指定医院体检产生的体检费用可自行报销,报销标准为100元/人,报销期限为其入职时间的3个月内()

XT5全系标配EPB电子驻车制动系统()

设备损坏引起水浸,由“谁管理,谁负责”实施,如属自来水公司负责,则由自来水公司负责抢修,物业公司提供协助;如属自管设备,自行组织力量抢修()

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!