重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

A.on

B.to

C.with

D.about

更多“The Finance Director argued _____ our Managing Director over profit sharing.”相关的问题

更多“The Finance Director argued _____ our Managing Director over profit sharing.”相关的问题

第1题

A.正确

B.错误

第2题

A.Y.是

B.N.否

第3题

A.Y.是

B.N.否

第4题

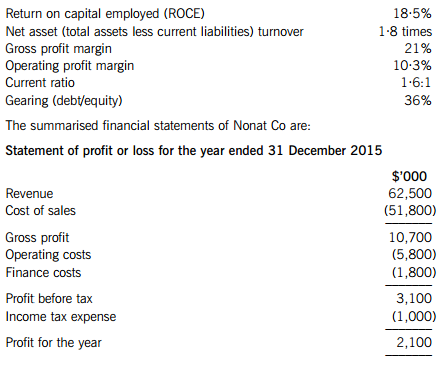

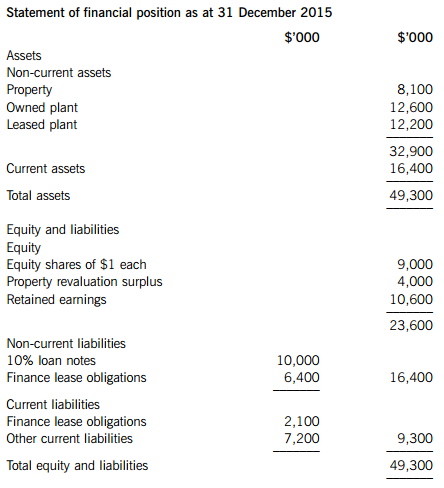

Required:

(a) Prepare for Nonat Co the equivalent ratios to those of its sector.

Note: The finance lease obligations should be treated as debt in the ROCE and gearing calculations. (6 marks)

(b) Analyse the financial performance and position of Nonat Co for the year to 31 December 2015 in comparison to the sector averages. (9 marks)

第5题

Which of the following statements, if any, is/are correct? (1) Internal auditors should report to the finance director as they understand internal controls and are best placed to implement any recommendations in a timely manner (2) Companies are not required to establish and maintain an internal audit function

A.1 only

B.2 only

C.Both 1 and 2

D.Neither 1 nor 2

第6题

You are the audit senior, and this is your first year on this audit. In order to familiarise yourself with Sunflower, the audit manager has asked you to undertake some research in order to gain an understanding of Sunflower, so that you are able to assist in the planning process. He has then asked that you identify relevant audit risks from the notes below and also consider how the team should respond to these risks.

Sunflower has spent $1·6 million in refurbishing all of its supermarkets; as part of this refurbishment programme their central warehouse has been extended and a smaller warehouse, which was only occasionally used, has been disposed of at a profit. In order to finance this refurbishment, a sum of $1·5 million was borrowed from the bank. This is due to be repaid over five years.

The company will be performing a year-end inventory count at the central warehouse as well as at all 25 supermarkets on 31 December. Inventory is valued at selling price less an average profit margin as the finance director believes that this is a close approximation to cost.

Prior to 2012, each of the supermarkets maintained their own financial records and submitted returns monthly to head office. During 2012 all accounting records have been centralised within head office. Therefore at the beginning of the year, each supermarket’s opening balances were transferred into head office’s accounting records. The increased workload at head office has led to some changes in the finance department and in November 2012 the financial controller left. His replacement will start in late December.

Required:

(a) List FIVE sources of information that would be of use in gaining an understanding of Sunflower Stores Co, and for each source describe what you would expect to obtain. (5 marks)

(b) Using the information provided, describe FIVE audit risks and explain the auditor’s response to each risk in planning the audit of Sunflower Stores Co. (10 marks)

(c) The finance director of Sunflower Stores Co is considering establishing an internal audit department. Required: Describe the factors the finance director should consider before establishing an internal audit department. (5 marks)

第7题

to be presented to shareholders at the forthcoming company general meeting. Uma has also commented that the

previous auditors did not use a liability disclaimer in their audit report, and would like more information about the use

of liability disclaimer paragraphs.

Required:

(b) Discuss the ethical issues raised by the request for your firm to type the financial statements of Blod Co.

(3 marks)

第8题

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

第9题

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

第10题

Section A暂缺

Section B – ALL SIX questions are compulsory and MUST be attempted

You are an audit manager of Pink Partners & Co (Pink) and are planning the audit of Golden Finance Co (Golden), a banking institution which provides a range of financial services including loans. Your firm has audited Golden for four years and the company’s year end is 30 September 2015.

At the end of August, Golden’s financial controller left and the new replacement is not due to start until approximately two months after the year end. The finance director, who is the sister-in-law of the audit engagement partner, has asked if a member of the audit team can be seconded to Golden for three months to act as the temporary financial controller.

You are aware that a number of the audit team members currently bank with Golden and two team members have significant loans owing to the company.

Pink’s taxation department also provides services to Golden. They have been approached by Golden to represent them in negotiations to resolve some outstanding issues with the taxation authorities, for which the fees quoted are substantial.

The finance director has informed the audit engagement partner that when the audit is complete, she would like the whole team to attend an evening watching the national football team play a match followed by a luxury meal.

Required:

Using the information above:

(i) Identify and explain FIVE ethical threats which may affect the independence of Pink Partners & Co’s audit of Golden Finance Co; and

(ii) For each threat, explain how it might be reduced to an acceptable level.

Note: The total marks will be split equally between each part.

相关内容

相关内容

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!