重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

(ii) The shares held in Date Inc and the dividend income received from that company. (7 marks)

更多“(ii) The shares held in Date Inc and the dividend income received from that company. (7 ma”相关的问题

更多“(ii) The shares held in Date Inc and the dividend income received from that company. (7 ma”相关的问题

第1题

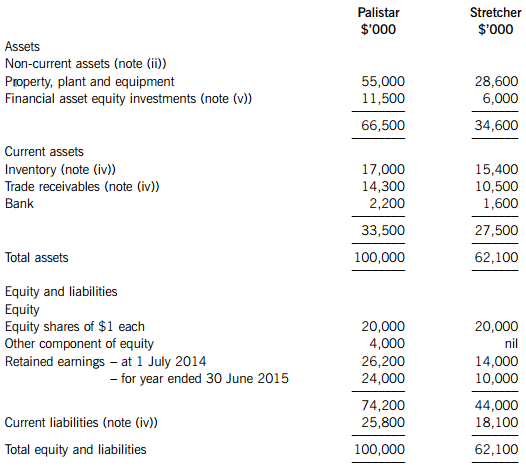

(a) On 1 January 2015, Palistar acquired 75% of Stretcher’s equity shares by means of an immediate share exchange of two shares in Palistar for five shares in Stretcher. The fair value of Palistar and Stretcher’s shares on 1 January 2015 were $4·00 and $3·00 respectively. In addition to the share exchange, Palistar will make a cash payment of $1·32 per acquired share, deferred until 1 January 2016. Palistar has not recorded any of the consideration for Stretcher in its financial statements. Palistar’s cost of capital is 10% per annum.

The summarised statements of financial position of the two companies as at 30 June 2015 are:

The following information is relevant:

(i) Stretcher’s business is seasonal and 60% of its annual profit is made in the period 1 January to 30 June each year.

(ii) At the date of acquisition, the fair value of Stretcher’s net assets was equal to their carrying amounts with the following exceptions:

An item of plant had a fair value of $2 million below its carrying value. At the date of acquisition it had a remaining life of two years.

The fair value of Stretcher’s investments was $7 million (see also note (v)).

Stretcher owned the rights to a popular mobile (cell) phone game. At the date of acquisition, a specialist valuer estimated that the rights were worth $12 million and had an estimated remaining life of five years.

(iii) Following an impairment review, consolidated goodwill is to be written down by $3 million as at 30 June 2015.

(iv) Palistar sells goods to Stretcher at cost plus 30%. Stretcher had $1·8 million of goods in its inventory at 30 June 2015 which had been supplied by Palistar. In addition, on 28 June 2015, Palistar processed the sale of $800,000 of goods to Stretcher, which Stretcher did not account for until their receipt on 2 July 2015. The in-transit reconciliation should be achieved by assuming the transaction had been recorded in the books of Stretcher before the year end. At 30 June 2015, Palistar had a trade receivable balance of $2·4 million due from Stretcher which differed to the equivalent balance in Stretcher’s books due to the sale made on 28 June 2015.

(v) At 30 June 2015, the fair values of the financial asset equity investments of Palistar and Stretcher were $13·2 million and $7·9 million respectively.

(vi) Palistar’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose Stretcher’s share price at that date is representative of the fair value of the shares held by the non-controlling interest.

Required:

Prepare the consolidated statement of financial position for Palistar as at 30 June 2015. (25 marks)

(b) For many years, Dilemma has owned 35% of the voting shares and held a seat on the board of Myno which has given Dilemma significant influence over Myno. The other shares (65%) in Myno were held by many other shareholders who all owned less than 10% of the share capital. On this basis, Dilemma considered Myno to be an associate and has used equity accounting to account for its investment.

In March 2015, Agresso made an offer to buy all of the shares of Myno. The offer was supported by the majority of Myno’s directors. Dilemma did not accept the offer and held on to its shares in Myno.

On 1 April 2015, Agresso announced that it had acquired the other 65% of the share capital of Myno and immediately convened a board meeting at which three of the previous directors of Myno were replaced, including the seat held by Dilemma.

Required:

Explain how the investment in Myno should be treated in the consolidated statement of profit or loss of Dilemma for the year ended 30 June 2015 and the consolidated statement of financial position at 30 June 2015. (5 marks)

第2题

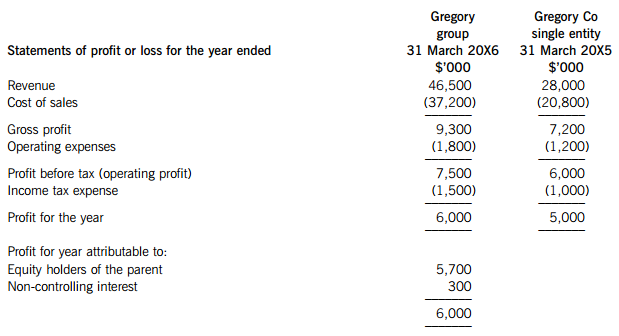

The summarised financial statements of Gregory Co as a single entity at 31 March 20X5 and as a group at 31 March 20X6 are:

Other information:

(i) Each month since the acquisition, Gregory Co’s sales to Tamsin Co were consistently $2m. Gregory Co had chosen to only make a gross profit margin of 10% on these sales as Tamsin Co is part of the group.

(ii) The values of property, plant and equipment held by both companies have been rising for several years.

(iii) On reviewing the above financial statements, Gregory Co’s chief executive officer (CEO) made the following observations:

(1) I see the profit for the year has increased by $1m which is up 20% on last year, but I thought it would be more as Tamsin Co was supposed to be a very profitable company.

(2) I have calculated the earnings per share (EPS) for 20X6 at 13 cents (6,000/46,000 x 100) and for 20X5 at 12·5 cents (5,000/40,000 x 100) and, although the profit has increased 20%, our EPS has barely changed.

(3) I am worried that the low price at which we are selling goods to Tamsin Co is undermining our group’s overall profitability.

(4) I note that our share price is now $2·30, how does this compare with our share price immediately before we bought Tamsin Co?

Required: (a) Reply to the four observations of the CEO. (8 marks)

(b) Using the above financial statements, calculate the following ratios for Gregory Co for the years ended 31 March 20X6 and 20X5 and comment on the comparative performance:

(i) Return on capital employed (ROCE)

(ii) Net asset turnover

(iii) Gross profit margin

(iv) Operating profit margin

Note: Four marks are available for the ratio calculations. (12 marks)

Note: Your answers to (a) and (b) should reflect the impact of the consolidation of Tamsin Co during the year ended 31 March 20X6.

第3题

英译中

The "shareholders" as such had no knowledge of the lives, thoughts or needs of the workmen employed by the company in which he held shares, and his influence on the relations of capital and labor was not good.

第4题

(ii) Advise Benny of the amount of tax he could save by delaying the sale of the shares by 30 days. For the

purposes of this part, you may assume that the benefit in respect of the furnished flat is £11,800 per

year. (3 marks)

第5题

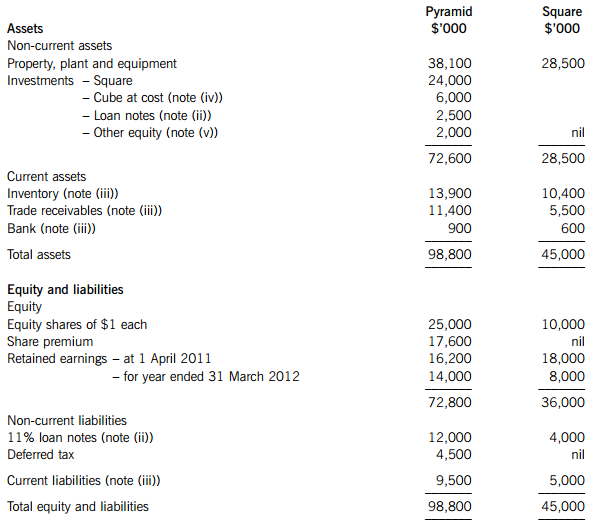

The summarised statements of financial position of the two companies as at 31 March 2012 are:

The following information is relevant:

(i) At the date of acquisition, Pyramid conducted a fair value exercise on Square’s net assets which were equal to their carrying amounts with the following exceptions:

– An item of plant had a fair value of $3 million above its carrying amount. At the date of acquisition it had a remaining life of five years. Ignore deferred tax relating to this fair value.

– Square had an unrecorded deferred tax liability of $1 million, which was unchanged as at 31 March 2012.

Pyramid’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose a share price for Square of $3·50 each is representative of the fair value of the shares held by the non-controlling interest.

(ii) Immediately after the acquisition, Square issued $4 million of 11% loan notes, $2·5 million of which were bought by Pyramid. All interest due on the loan notes as at 31 March 2012 has been paid and received.

(iii) Pyramid sells goods to Square at cost plus 50%. Below is a summary of the recorded activities for the year ended 31 March 2012 and balances as at 31 March 2012:

On 26 March 2012, Pyramid sold and despatched goods to Square, which Square did not record until they were received on 2 April 2012. Square’s inventory was counted on 31 March 2012 and does not include any goods purchased from Pyramid.

On 27 March 2012, Square remitted to Pyramid a cash payment which was not received by Pyramid until 4 April 2012. This payment accounted for the remaining difference on the current accounts.

(iv) Pyramid bought 1·5 million shares in Cube on 1 October 2011; this represents a holding of 30% of Cube’s equity. At 31 March 2012, Cube’s retained profits had increased by $2 million over their value at 1 October 2011. Pyramid uses equity accounting in its consolidated financial statements for its investment in Cube.

(v) The other equity investments of Pyramid are carried at their fair values on 1 April 2011. At 31 March 2012, these had increased to $2·8 million.

(vi) There were no impairment losses within the group during the year ended 31 March 2012.

Required:

Prepare the consolidated statement of financial position for Pyramid as at 31 March 2012.

第6题

2005. The financial statements were authorised on 12 December 2005. The following events are relevant to the

financial statements for the year ended 31 October 2005:

(i) Ryder has a good record of ordinary dividend payments and has adopted a recent strategy of increasing its

dividend per share annually. For the last three years the dividend per share has increased by 5% per annum.

On 20 November 2005, the board of directors proposed a dividend of 10c per share for the year ended

31 October 2005. The shareholders are expected to approve it at a meeting on 10 January 2006, and a

dividend amount of $20 million will be paid on 20 February 2006 having been provided for in the financial

statements at 31 October 2005. The directors feel that a provision should be made because a ‘valid expectation’

has been created through the company’s dividend record. (3 marks)

(ii) Ryder disposed of a wholly owned subsidiary, Krup, a public limited company, on 10 December 2005 and made

a loss of $9 million on the transaction in the group financial statements. As at 31 October 2005, Ryder had no

intention of selling the subsidiary which was material to the group. The directors of Ryder have stated that there

were no significant events which have occurred since 31 October 2005 which could have resulted in a reduction

in the value of Krup. The carrying value of the net assets and purchased goodwill of Krup at 31 October 2005

were $20 million and $12 million respectively. Krup had made a loss of $2 million in the period 1 November

2005 to 10 December 2005. (5 marks)

(iii) Ryder acquired a wholly owned subsidiary, Metalic, a public limited company, on 21 January 2004. The

consideration payable in respect of the acquisition of Metalic was 2 million ordinary shares of $1 of Ryder plus

a further 300,000 ordinary shares if the profit of Metalic exceeded $6 million for the year ended 31 October

2005. The profit for the year of Metalic was $7 million and the ordinary shares were issued on 12 November

2005. The annual profits of Metalic had averaged $7 million over the last few years and, therefore, Ryder had

included an estimate of the contingent consideration in the cost of the acquisition at 21 January 2004. The fair

value used for the ordinary shares of Ryder at this date including the contingent consideration was $10 per share.

The fair value of the ordinary shares on 12 November 2005 was $11 per share. Ryder also made a one for four

bonus issue on 13 November 2005 which was applicable to the contingent shares issued. The directors are

unsure of the impact of the above on earnings per share and the accounting for the acquisition. (7 marks)

(iv) The company acquired a property on 1 November 2004 which it intended to sell. The property was obtained

as a result of a default on a loan agreement by a third party and was valued at $20 million on that date for

accounting purposes which exactly offset the defaulted loan. The property is in a state of disrepair and Ryder

intends to complete the repairs before it sells the property. The repairs were completed on 30 November 2005.

The property was sold after costs for $27 million on 9 December 2005. The property was classified as ‘held for

sale’ at the year end under IFRS5 ‘Non-current Assets Held for Sale and Discontinued Operations’ but shown at

the net sale proceeds of $27 million. Property is depreciated at 5% per annum on the straight-line basis and no

depreciation has been charged in the year. (5 marks)

(v) The company granted share appreciation rights (SARs) to its employees on 1 November 2003 based on ten

million shares. The SARs provide employees at the date the rights are exercised with the right to receive cash

equal to the appreciation in the company’s share price since the grant date. The rights vested on 31 October

2005 and payment was made on schedule on 1 December 2005. The fair value of the SARs per share at

31 October 2004 was $6, at 31 October 2005 was $8 and at 1 December 2005 was $9. The company has

recognised a liability for the SARs as at 31 October 2004 based upon IFRS2 ‘Share-based Payment’ but the

liability was stated at the same amount at 31 October 2005. (5 marks)

Required:

Discuss the accounting treatment of the above events in the financial statements of the Ryder Group for the year

ended 31 October 2005, taking into account the implications of events occurring after the balance sheet date.

(The mark allocations are set out after each paragraph above.)

(25 marks)

第7题

(ii) Explain, with reasons, the relief available in respect of the fall in value of the shares in All Over plc,

identify the years in which it can be claimed and state the time limit for submitting the claim.

(3 marks)

第8题

estate and is seeking advice on his father’s capital gains tax position and the payment of inheritance tax following his

death.

The following information has been extracted from client files and from telephone conversations with Crusoe.

Noland – personal information:

– Divorcee whose only other relatives are his sister, Avril, and two grandchildren.

– Died suddenly on 1 October 2007 without having made a will.

– Under the laws of intestacy, the whole of his estate passes to Crusoe.

Noland – income tax and capital gains tax:

– Has been a basic rate taxpayer since the tax year 2000/01.

– Sales of quoted shares resulted in:

– Chargeable gains of £7,100 and allowable losses of £17,800 in the tax year 2007/08.

– Chargeable gains of approximately £14,000 each tax year from 2000/01 to 2006/07.

– None of the shares were held for long enough to qualify for taper relief.

Noland – gifts made during lifetime:

– On 1 December 1999 Noland gave his house to Crusoe.

– Crusoe has allowed Noland to continue living in the house and has charged him rent of £120 per month

since 1 December 1999. The market rent for the house would be £740 per month.

– The house was worth £240,000 at the time of the gift and £310,000 on 1 October 2007.

– On 1 November 2004 Noland transferred quoted shares worth £232,000 to a discretionary trust for the benefit

of his grandchildren.

Noland – probate values of assets held at death: £

– Portfolio of quoted shares 370,000

Shares in Kurb Ltd 38,400

Chattels and cash 22,300

Domestic liabilities including income tax payable (1,900)

– It should be assumed that these values will not change for the foreseeable future.

Kurb Ltd:

– Unquoted trading company

– Noland purchased the shares on 1 December 2005.

Crusoe:

– Long-standing personal tax client of your firm.

– Married with two young children.

– Successful investment banker with very high net worth.

– Intends to gift the portfolio of quoted shares inherited from Noland to his aunt, Avril, who has very little personal

wealth.

Required:

(a) Prepare explanatory notes together with relevant supporting calculations in order to quantify the tax relief

potentially available in respect of Noland’s capital losses realised in 2007/08. (4 marks)

第9题

(ii) Explain the income tax (IT), national insurance (NIC) and capital gains tax (CGT) implications arising on

the grant to and exercise by an employee of an option to buy shares in an unapproved share option

scheme and on the subsequent sale of these shares. State clearly how these would apply in Henry’s

case. (8 marks)

第10题

(ii) Calculate Paul’s tax liability if he exercises the share options in Memphis plc and subsequently sells the

shares in Memphis plc immediately, as proposed, and show how he may reduce this tax liability.

(4 marks)

相关内容

相关内容

发站给中途站预留的包房,可利用其发售最远至预留站的车票()

执勤分队集体外出活动.除当班哨兵外.营区至少保留三班哨的兵力()

骑士小张送餐多了发现有时候顾客不方便出来当面接收货品,小张总结下来觉得送到门卫处/前台/门口等指定的位置后跟客户再三确认是否无误,还得用水印相机拍照通过APP“消息”发给顾客,这样就万无一失了,小张的做法对吗()

新员工入职,按照公司要求到指定医院体检产生的体检费用可自行报销,报销标准为100元/人,报销期限为其入职时间的3个月内()

XT5全系标配EPB电子驻车制动系统()

设备损坏引起水浸,由“谁管理,谁负责”实施,如属自来水公司负责,则由自来水公司负责抢修,物业公司提供协助;如属自管设备,自行组织力量抢修()

发站给中途站预留的包房,可利用其发售最远至预留站的车票()

执勤分队集体外出活动.除当班哨兵外.营区至少保留三班哨的兵力()

骑士小张送餐多了发现有时候顾客不方便出来当面接收货品,小张总结下来觉得送到门卫处/前台/门口等指定的位置后跟客户再三确认是否无误,还得用水印相机拍照通过APP“消息”发给顾客,这样就万无一失了,小张的做法对吗()

新员工入职,按照公司要求到指定医院体检产生的体检费用可自行报销,报销标准为100元/人,报销期限为其入职时间的3个月内()

XT5全系标配EPB电子驻车制动系统()

设备损坏引起水浸,由“谁管理,谁负责”实施,如属自来水公司负责,则由自来水公司负责抢修,物业公司提供协助;如属自管设备,自行组织力量抢修()

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!