重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

On the assumption that Ambel Co is an associate of Caddy Co, what would be the carrying amount of the investment in Ambel Co in the consolidated statement of financial position of Caddy Co as at 30 September 20X5?

A、$1,560,000

B、$1,395,000

C、$1,515,000

D、$1,690,000

更多“Caddy Co acquired 240,000 of Ambel Co’s 800,000 equity shares for $6 per share on 1 O”相关的问题

更多“Caddy Co acquired 240,000 of Ambel Co’s 800,000 equity shares for $6 per share on 1 O”相关的问题

第1题

On 1 October 20X4, Flash Co acquired an item of plant under a five-year lease agreement. The plant had a cash purchase cost of $25m. The agreement had an implicit finance cost of 10% per annum and required an immediate deposit of $2m and annual rentals of $6m paid on 30 September each year for five years.

What is the current liability for the leased plant in Flash Co’s statement of financial position as at 30 September 20X5?

A、$19,300,000

B、$4,070,000

C、$5,000,000

D、$3,850,000

第2题

At what amount should the non-controlling interests in Square Co be valued in the consolidated statement of financial position of the Pyramid group as at 30 September 20X5?

A、$26,680,000

B、$7,900,000

C、$7,780,000

D、$12,220,000

第3题

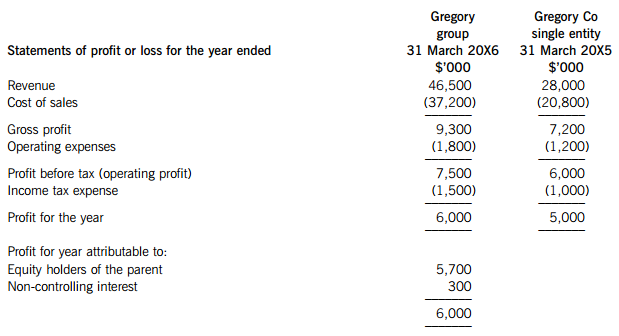

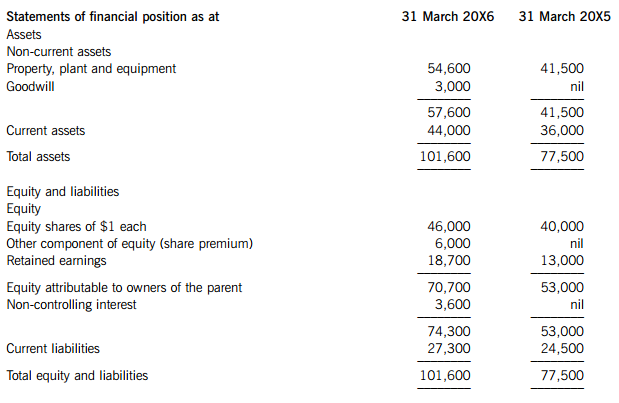

The summarised financial statements of Gregory Co as a single entity at 31 March 20X5 and as a group at 31 March 20X6 are:

Other information:

(i) Each month since the acquisition, Gregory Co’s sales to Tamsin Co were consistently $2m. Gregory Co had chosen to only make a gross profit margin of 10% on these sales as Tamsin Co is part of the group.

(ii) The values of property, plant and equipment held by both companies have been rising for several years.

(iii) On reviewing the above financial statements, Gregory Co’s chief executive officer (CEO) made the following observations:

(1) I see the profit for the year has increased by $1m which is up 20% on last year, but I thought it would be more as Tamsin Co was supposed to be a very profitable company.

(2) I have calculated the earnings per share (EPS) for 20X6 at 13 cents (6,000/46,000 x 100) and for 20X5 at 12·5 cents (5,000/40,000 x 100) and, although the profit has increased 20%, our EPS has barely changed.

(3) I am worried that the low price at which we are selling goods to Tamsin Co is undermining our group’s overall profitability.

(4) I note that our share price is now $2·30, how does this compare with our share price immediately before we bought Tamsin Co?

Required: (a) Reply to the four observations of the CEO. (8 marks)

(b) Using the above financial statements, calculate the following ratios for Gregory Co for the years ended 31 March 20X6 and 20X5 and comment on the comparative performance:

(i) Return on capital employed (ROCE)

(ii) Net asset turnover

(iii) Gross profit margin

(iv) Operating profit margin

Note: Four marks are available for the ratio calculations. (12 marks)

Note: Your answers to (a) and (b) should reflect the impact of the consolidation of Tamsin Co during the year ended 31 March 20X6.

第4题

(b) You are the audit manager of Johnston Co, a private company. The draft consolidated financial statements for

the year ended 31 March 2006 show profit before taxation of $10·5 million (2005 – $9·4 million) and total

assets of $55·2 million (2005 – $50·7 million).

Your firm was appointed auditor of Tiltman Co when Johnston Co acquired all the shares of Tiltman Co in March

2006. Tiltman’s draft financial statements for the year ended 31 March 2006 show profit before taxation of

$0·7 million (2005 – $1·7 million) and total assets of $16·1 million (2005 – $16·6 million). The auditor’s

report on the financial statements for the year ended 31 March 2005 was unmodified.

You are currently reviewing two matters that have been left for your attention on the audit working paper files for

the year ended 31 March 2006:

(i) In December 2004 Tiltman installed a new computer system that properly quantified an overvaluation of

inventory amounting to $2·7 million. This is being written off over three years.

(ii) In May 2006, Tiltman’s head office was relocated to Johnston’s premises as part of a restructuring.

Provisions for the resulting redundancies and non-cancellable lease payments amounting to $2·3 million

have been made in the financial statements of Tiltman for the year ended 31 March 2006.

Required:

Identify and comment on the implications of these two matters for your auditor’s reports on the financial

statements of Johnston Co and Tiltman Co for the year ended 31 March 2006. (10 marks)

第5题

(b) You are an audit manager in a firm of Chartered Certified Accountants currently assigned to the audit of Cleeves

Co for the year ended 30 September 2006. During the year Cleeves acquired a 100% interest in Howard Co.

Howard is material to Cleeves and audited by another firm, Parr & Co. You have just received Parr’s draft

auditor’s report for the year ended 30 September 2006. The wording is that of an unmodified report except for

the opinion paragraph which is as follows:

Audit opinion

As more fully explained in notes 11 and 15 impairment losses on non-current assets have not been

recognised in profit or loss as the directors are unable to quantify the amounts.

In our opinion, provision should be made for these as required by International Accounting Standard 36

(Impairment). If the provision had been so recognised the effect would have been to increase the loss before

and after tax for the year and to reduce the value of tangible and intangible non-current assets. However,

as the directors are unable to quantify the amounts we are unable to indicate the financial effect of such

omissions.

In view of the failure to provide for the impairments referred to above, in our opinion the financial statements

do not present fairly in all material respects the financial position of Howard Co as of 30 September 2006

and of its loss and its cash flows for the year then ended in accordance with International Financial Reporting

Standards.

Your review of the prior year auditor’s report shows that the 2005 audit opinion was worded identically.

Required:

(i) Critically appraise the appropriateness of the audit opinion given by Parr & Co on the financial

statements of Howard Co, for the years ended 30 September 2006 and 2005. (7 marks)

相关内容

相关内容

On 1 October 20X4, Pyramid Co acquired 80% of Square Co’s 9 million equity shares. At

On 1 October 20X4, Kalatra Co commenced drilling for oil from an undersea oilfield. Ka

Consolidated financial statements are presented on the basis that the companies within

When a parent is evaluating the assets of a potential subsidiary, certain intangible a

Gregory Co is a listed company and, until 1 October 20X5, it had no subsidiaries. On that

(a) A director of Enca, a public listed company, has expressed concerns about the accounti

On 1 October 20X4, Pyramid Co acquired 80% of Square Co’s 9 million equity shares. At

On 1 October 20X4, Kalatra Co commenced drilling for oil from an undersea oilfield. Ka

Consolidated financial statements are presented on the basis that the companies within

When a parent is evaluating the assets of a potential subsidiary, certain intangible a

Gregory Co is a listed company and, until 1 October 20X5, it had no subsidiaries. On that

(a) A director of Enca, a public listed company, has expressed concerns about the accounti

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!