重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

Introduction

The country of Mahem is in a long and deep economic recession with unemployment at its highest since the country became an independent nation. In an attempt to stimulate the economy the government has launched a Private/Public investment policy where the government invests in capital projects with the aim of stimulating the involvement of private sector firms. The building of a new community centre in the industrial city of Tillo is an example of such an initiative. Community centres are central to the culture of Mahem. They are designed as places where people can meet socially, local organisations can hold conferences and meetings and farmers can sell their produce to the local community. The centres are seen as contributing to a vibrant community life. The community centre in Tillo is in a sprawling old building rented (at $12,000 per month) from a local landowner. The current community centre is also relatively energy inefficient.

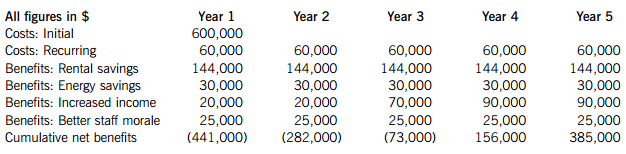

In 2010 a business case was put forward to build a new centre on local authority owned land on the outskirts of Tillo. The costs and benefits of the business case are shown in Figure 1. As required by the Private/Public investment policy the project showed payback during year four of the investment.

Figure 1: Costs and benefits of the business case for the community centre at Tillo

New buildings built under the Private/Public investment policy must attain energy level targets and this is the basis for the estimation, above, of the energy savings. It is expected that the new centre will attract more customers who will pay for the centre’s use as well as increasing the use of facilities such as the cafeteria, shop and business centre. These benefits are estimated, above, under increased income. Finally, it is felt that staff will be happier in the new building and their motivation and morale will increase. The centre currently employs 20 staff, 16 of whom have been with the centre for more than five years. All employees were transferred from the old to the new centre. These benefits are shown as better staff morale in Figure 1.

Construction of the centre 2010–2011

In October 2010 the centre was commissioned with a planned delivery date of June 2011 at a cost of $600,000 (as per Figure 1). Building the centre went relatively smoothly. Progress was monitored and issues resolved in monthly meetings between the company constructing the centre and representatives of the local authority. These meetings focused on the building of the centre, monitoring progress and resolving issues. Most of these issues were relatively minor because requirements were well specified in standard architectural drawings originally agreed between the project sponsor and the company constructing the centre. Unfortunately, the original project sponsor (an employee of the local authority) who had been heavily involved in the initial design, suffered ill health and died in April 2011. The new project sponsor (again an employee of the local authority) was less enthusiastic about the project and began to raise a number of objections. Her first concern was that the construction company had used sub-contracted labour and had sourced less than 80% of timber used in the building from sustainable resources. She pointed out the contractual terms of supply for the Private/Public policy investment initiatives mandated that sub-contracting was not allowed without the local authority’s permission and that at least 80% of the timber used must come from sustainable forests. The company said that this had not been brought to their attention at the start of the project. However, they would try to comply with these requirements for the rest of the contract. The new sponsor also refused to sign off acceptance of the centre because of the poor quality of the internal paintwork. The construction company explained that this was the intended finish quality of the centre and had been agreed with the previous sponsor. They produced a letter to verify this. However, the letter was not counter-signed by the sponsor and so its validity was questioned. In the end, the construction company agreed to improve the internal painting at their own cost. The new sponsor felt that she had delivered ‘value for money’ by challenging the construction company. Despite this problem with the internal painting, the centre was finished in May 2011 at a cost of $600,000. The centre also included disability access built at the initiative of the construction company. It had found it difficult to find local authority staff willing and able to discuss disability access and so it was therefore left alone to interpret relevant legal requirements. Fortunately, their interpretation was correct and the new centre was deemed, by an independent assessor, to meet accessibility requirements.

Unfortunately, the new centre was not as successful as had been predicted, with income in the first year well below expectations. The project sponsor began to be increasingly critical of the builders of the centre and questioned the whole value of the project. She was openly sceptical of the project to her fellow local authority employees. She suggested that the project to build a cost-effective centre had failed and called for an inquiry into the performance of the project manager of the construction company who was responsible for building the centre. ‘We need him to explain to us why the centre is not delivering the benefits we expected’, she explained.

Required:

(a) The local authority has commissioned the independent Project Audit Agency (PAA) to look into how the project had been commissioned and managed. The PAA believes that a formal ‘terms of reference’ or ‘project initiation document’ would have resolved or clarified some of the problems and issues encountered in the project. It also feels that there are important lessons to be learnt by both the local authority and the construction company.

Analyse how a formal ‘terms of reference’ (project initiation document) would have helped address problems encountered in the project to construct the community centre and lead to improved project management in future projects. (13 marks)

(b) The PAA also believes that the four sets of benefits identified in the original business case (rental savings, energy savings, increased income and better staff morale) should have been justified more explicitly.

Draft an analysis for the PAA that formally categorises and critically evaluates each of the four sets of proposed benefits defined in the original business case. (12 marks)

更多“IntroductionThe country of Mahem is in a long and deep economic recession with unemploymen”相关的问题

更多“IntroductionThe country of Mahem is in a long and deep economic recession with unemploymen”相关的问题

第2题

A. It used to being

B. It used to be

C. It is used to being

D. It is used to be

第3题

A.count

B.subtract

C.calculate

D.multiply

第4题

(36 ) “ 查询选修了 3 门以上课程的学生的学生号 ” ,正确的 SQL 语句是

A) SELECT S# FROM SC GEOUPBY S# WHERE COUN (* ) 〉 3

B) SELECT S# FROM SC GEOUPBY S# HAVING COUN (* ) 〉 3

C) SELECT S# FROM SC ORDER S# HAVING COUN (* ) 〉 3

D) SELECT S# FROM SC ORDER S# WHERE COUN (* ) 〉 3

第5题

I wish you would give me a more detailed ()of you trip.

A、account

B、advance

C、accuse

D、count

第6题

(c) Identify and discuss the ethical and professional matters raised at the inventory count of LA Shots Co.

(6 marks)

第7题

It would bring about an()of the conditions of the working men and women in this country.

A.advance

B.increase

C.improvement

D.achievement

第8题

分析以下程序,判断程序段执行完毕后,AX=______,BL=______。

DA1 DW 1234H, 5678H

DA2 DB 12H, 34H

COUNT EQU $-DA1

…

MOV CL, COUNT

MOV AX, WORD PTR DA2

MOV BL, BYTE PTR DA1+1

HLT

第9题

A.Toy::count

B.Toy.countCcount

C.obj.count

第10题

Efforts by commercial banks and financial () have gone a long way to improve the country's banking industry in recent years.近年来商业银行和金融监督机构为改善我国的银行业已经付出了很多努力。

A、supervizedog

B、watchdogs

C、dogwatch

D、dogsupervize

第11题

下面程序的正确输出是()。 public class Hello { public static void main(String args[]) { int count, xPos=25; for (count=1; count<=10; count++ ) { if (count==5 ) break; System.out.println(count ); xPos += 10; } } }

A.1 2 3 4

B.1 3 4

C.编译错误

D.以上都不是

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!