重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

Debt covenants to protect bondholders areleast likely to:

A.restrict the issuance of new debt.

B.require sinking fund redemptions.

C.prohibit bond repurchases at a premium to par.

更多“Debt covenants to protect bondholders areleast likely to:A.restrict the issuance of new”相关的问题

更多“Debt covenants to protect bondholders areleast likely to:A.restrict the issuance of new”相关的问题

第1题

Which of the following is most likely a benefit of debt covenants for the borrower?

A.Reduction in the cost of borrowing.

B.Limitations on the company’s ability to pay dividends.

C.Restrictions on how the borrowed money may be invested.

第2题

An analyst reviews a corporate bond indenture that contains these two covenants:

1) The borrower will pay interest semi-annually

and principal at maturity.

2) The borrower will not incur additional debt if its debt/capital ratio is more than 50%.

What types of covenants are these?

A. Both are affirmative covenants.

B. Covenant 1 is negative and Covenant 2 is affirmative.

C. Covenant 2 is negative and Covenant 1 is affirmative.

第3题

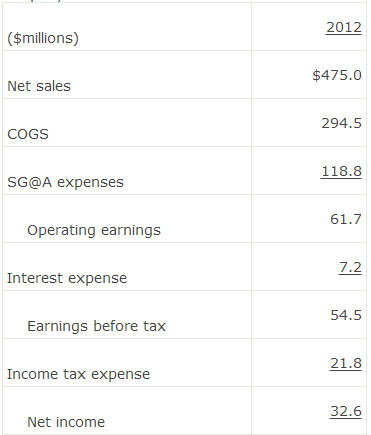

The 2012 income statement for a subject company is as follows:

For 2013, net sales are projected to increase by 12%, gross profit margin is expected to increase by 2% while SG&A expenses as a percent of net sales is expected to remain constant, total debt is not expected to change, and the effective tax rate is expected to remain constant.

Based on the above information, the company’s 2013 projected net income (in millions) is closest to:

A. $33.

B. $44.

C. $55.

第4题

A.A covenant is a conditional promise to perform

B.A conditional promise becomes a covenant if the condition is met

C.A contract cannot contain conditions to excuse performance

D.A party cannot sue over breach of a covenant by the other party

第6题

well managed and the group accounting policies are rigorously applied. The company’s financial year end is

31 December.

Prescott has been seeking to acquire a construction company for some time in order to bring in-house the building

and refurbishment of hotels and related leisure facilities (e.g. swimming pools, squash courts and restaurants).

Prescott’s management has recently identified Robson Construction Co as a potential target and has urgently requested

that you undertake a limited due diligence review lasting two days next week.

Further to their preliminary talks with Robson’s management, Prescott has provided you with the following brief on

Robson Construction Co:

The chief executive, managing director and finance director are all family members and major shareholders. The

company name has an established reputation for quality constructions.

Due to a recession in the building trade the company has been operating at its overdraft limit for the last 18

months and has been close to breaching debt covenants on several occasions.

Robson’s accounting policies are generally less prudent than those of Prescott (e.g. assets are depreciated over

longer estimated useful lives).

Contract revenue is recognised on the percentage of completion method, measured by reference to costs incurred

to date. Provisions are made for loss-making contracts.

The company’s management team includes a qualified and experienced quantity surveyor. His main

responsibilities include:

(1) supervising quarterly physical counts at major construction sites;

(2) comparing costs to date against quarterly rolling budgets; and

(3) determining profits and losses by contract at each financial year end.

Although much of the labour is provided under subcontracts all construction work is supervised by full-time site

managers.

In August 2005, Robson received a claim that a site on which it built a housing development in 2002 was not

properly drained and is now subsiding. Residents are demanding rectification and claiming damages. Robson

has referred the matter to its lawyers and denied all liability, as the site preparation was subcontracted to Sarwar

Services Co. No provisions have been made in respect of the claims, nor has any disclosure been made.

The auditor’s report on Robson’s financial statements for the year to 30 June 2005 was signed, without

modification, in March 2006.

Required:

(a) Identify and explain the specific matters to be clarified in the terms of engagement for this due diligence

review of Robson Construction Co. (6 marks)

第7题

单句理解

听力原文:More common for lending transactions today is compound interest.

(1)

A.Lending covenants now are often made at compound interest.

B.Lending transactions now are often made at compound interest.

C.Lending decisions now are often made at compound interest.

D.Lending proposals now are often made at compound interest.

第10题

相关内容

相关内容

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是()。

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“金降落伞”策略。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“焦土策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“白衣骑士”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“毒丸策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略不是()。

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是()。

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“金降落伞”策略。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“焦土策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“白衣骑士”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略是“毒丸策略”。()

目标公司董事会决议:目标公司向普通股股东发行优先股,一旦公司被收购,股东持有的优先股就可以转换为一定数额的收购方股票。这种反收购策略不是()。

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!