重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

更多“If there’s any profit to be got out of the deal, I’m going to be in on it.如果这次买卖可以赚到钱,我打算凑一份。()”相关的问题

更多“If there’s any profit to be got out of the deal, I’m going to be in on it.如果这次买卖可以赚到钱,我打算凑一份。()”相关的问题

第1题

Section B – TWO questions ONLY to be attempted

(a) Cate is an entity in the software industry. Cate had incurred substantial losses in the fi nancial years 31 May 2004 to 31 May 2009. In the fi nancial year to 31 May 2010 Cate made a small profi t before tax. This included signifi cant non-operating gains. In 2009, Cate recognised a material deferred tax asset in respect of carried forward losses, which will expire during 2012. Cate again recognised the deferred tax asset in 2010 on the basis of anticipated performance in the years from 2010 to 2012, based on budgets prepared in 2010. The budgets included high growth rates in profi tability. Cate argued that the budgets were realistic as there were positive indications from customers about future orders. Cate also had plans to expand sales to new markets and to sell new products whose development would be completed soon. Cate was taking measures to increase sales, implementing new programs to improve both productivity and profi tability. Deferred tax assets less deferred tax liabilities represent 25% of shareholders’ equity at 31 May 2010. There are no tax planning opportunities available to Cate that would create taxable profi t in the near future. (5 marks)

(b) At 31 May 2010 Cate held an investment in and had a signifi cant infl uence over Bates, a public limited company. Cate had carried out an impairment test in respect of its investment in accordance with the procedures prescribed in IAS 36, Impairment of assets. Cate argued that fair value was the only measure applicable in this case as value-in-use was not determinable as cash fl ow estimates had not been produced. Cate stated that there were no plans to dispose of the shareholding and hence there was no binding sale agreement. Cate also stated that the quoted share price was not an appropriate measure when considering the fair value of Cate’s signifi cant infl uence on Bates. Therefore, Cate estimated the fair value of its interest in Bates through application of two measurement techniques; one based on earnings multiples and the other based on an option–pricing model. Neither of these methods supported the existence of an impairment loss as of 31 May 2010. (5 marks)

(c) At 1 April 2009 Cate had a direct holding of shares giving 70% of the voting rights in Date. In May 2010, Date issued new shares, which were wholly subscribed for by a new investor. After the increase in capital, Cate retained an interest of 35% of the voting rights in its former subsidiary Date. At the same time, the shareholders of Date signed an agreement providing new governance rules for Date. Based on this new agreement, Cate was no longer to be represented on Date’s board or participate in its management. As a consequence Cate considered that its decision not to subscribe to the issue of new shares was equivalent to a decision to disinvest in Date. Cate argued that the decision not to invest clearly showed its new intention not to recover the investment in Date principally through continuing use of the asset and was considering selling the investment. Due to the fact that Date is a separate line of business (with separate cash fl ows, management and customers), Cate considered that the results of Date for the period to 31 May 2010 should be presented based on principles provided by IFRS 5 Non-current Assets Held for Sale and Discontinued Operations. (8 marks)

(d) In its 2010 fi nancial statements, Cate disclosed the existence of a voluntary fund established in order to provide a post-retirement benefi t plan (Plan) to employees. Cate considers its contributions to the Plan to be voluntary, and has not recorded any related liability in its consolidated fi nancial statements. Cate has a history of paying benefi ts to its former employees, even increasing them to keep pace with infl ation since the commencement of the Plan. The main characteristics of the Plan are as follows:

(i) the Plan is totally funded by Cate;

(ii) the contributions for the Plan are made periodically;

(iii) the post retirement benefi t is calculated based on a percentage of the fi nal salaries of Plan participants dependent on the years of service;

(iv) the annual contributions to the Plan are determined as a function of the fair value of the assets less the liability arising from past services.

Cate argues that it should not have to recognise the Plan because, according to the underlying contract, it can terminate its contributions to the Plan, if and when it wishes. The termination clauses of the contract establish that Cate must immediately purchase lifetime annuities from an insurance company for all the retired employees who are already receiving benefi t when the termination of the contribution is communicated. (5 marks)

Required:

Discuss whether the accounting treatments proposed by the company are acceptable under International Financial Reporting Standards.

Professional marks will be awarded in this question for clarity and quality of discussion. (2 marks)

The mark allocation is shown against each of the four parts above.

第2题

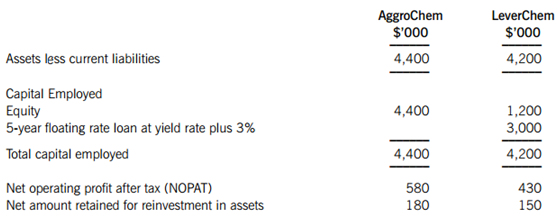

AggroChem is a fully listed company fi nanced wholly by equity. LeverChem is listed on an alternative investment market. Both companies have been trading for over 10 years and have shown strong levels of profi tability recently. However, both companies’ shares are thinly traded. It is thought that the current market value of LeverChem’s shares at higher than the book value is accurate, but it is felt that AggroChem shares are not quoted accurately by the market.

higher than the book value is accurate, but it is felt that AggroChem shares are not quoted accurately by the market.

The following information is taken from the fi nancial statements of both companies at the start of the current year:

It can be assumed that the retained earnings for both companies are equal to the net reinvestment in assets.

The assets of both companies are stated at fair value. Discussions with the AtReast Bank have led to an agreement that the fl oating rate loan to LeverChem can be transferred to the combined business on the same terms. The current yield rate is 5% and the current equity risk premium is 6%. It can be assumed that the risk free rate of return is equivalent to the yield rate. AggroChem’s beta has been estimated to be 1·26.

AggroChem Co wants to use the Black-Scholes option pricing (BSOP) model to assess the value of the combined business and the maximum premium payable to LeverChem’s shareholders. AggroChem has conducted a review of the volatility of the NOPAT values of both companies since both were formed and has estimated that the volatility of the combined business assets, if the acquisition were to go ahead, would be 35%. The exercise price should be calculated as the present value of a discount (zero-coupon) bond with an identical yield and term to maturity of the current bond.

Required:

Prepare a report for the management of AggroChem on the valuation of the combined business following acquisition and the maximum premium payable to the shareholders of LeverChem. Your report should:

(i) Using the free cash fl ow model, estimate the market value of equity for AggroChem Co, explaining any assumptions made. (9 marks)

(ii) Explain the circumstances in which the Black-Scholes option pricing (BSOP) model could be used to assess the value of a company, including the data required for the variables used in the model. (5 marks)

(iii) Using the BSOP methodology, estimate the maximum price and premium AggroChem may pay for LeverChem. (9 marks)

(iv) Discuss the appropriateness of the method used in part (iii) above, by considering whether the BSOP model can provide a meaningful value for a company. (5 marks)

Professional marks will be awarded in question 2 for the clarity and presentation of the report. (4 marks)

第4题

Undervaluation of closing stock may lead to ______.

A.higher profit than actual

B.less profit than actual

C.higher tax payable

D.none of the above

第5题

解释一个竞争性的、追求利润最大化的企业如何决定每种生产要素需要多少。

Explain how a competitive, profit-maximizing firm decides how much of each factor of production to demand.

第6题

There's no use (bargain) ______ any more. It's a fixed price.

第7题

It's a very old car and the spare parts are _________ available.

A. no any longer

B. no longer

C. not any longer

D. no more

第10题

They have never heard any _______.

A.a customer complaint

B.the customer's complaints

C.customer's complaint

D.the customers' complaints

相关内容

相关内容

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!