重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

Pursuant ()the results ()the research, we have canceled out assumptions.

A、to,of

B、on,of

C、to,for

D、on

E、for

更多“Pursuant ()the results ()the research, we have canceled out assumptions.A、to,ofB、on,o”相关的问题

更多“Pursuant ()the results ()the research, we have canceled out assumptions.A、to,ofB、on,o”相关的问题

第1题

Protests are possible and shall be resolved under FINA rule GR 9.2.2 and GR 9.2.3.Protests must be submitted to the referee in writing by the Team Leader,with a deposit of 100 Swiss Francs or its equivalent,within 30 minutes following the conclusion of the respective competition.The referee shall consider all protests.If he rejects the protest,he must state the reasons for his decision.

第2题

下列语句片段: int result; int a=17,b=6; result=(a%b>4) ? a%b:a/b; System.out.println(result);

A.0

B.1

C.2

D.5

第3题

材料:

If,by reason of or in compliance with any such directions or recommendations,the vessel does not proceed to the port or ports named in the Bill of Lading or to which she may have been ordered pursuant thereto,the Vessel may proceed to any port as directed or recommended or to any safe port which the Owners in their discretion may decide on and there discharge the cargo.Such discharge shall be deemed to be due fulfillment of the contract of affreightment and the Owners shall be entitled to freight as if discharge had been effected at the port or ports named in the Bill of Lading or to which the Vessel may have been ordered pursuant thereto.

问题:

If the vessel does not, under the directions of the Charterer, proceed to the port or ports named in the Bill of Lading or to which she may have been ordered pursuant thereto to, she may proceed to all the following ports except ______ .

A.any port as directed

B.any port as recommended

C.any safe port which the Owners in their discretion may decide on

D.the port or ports of origin

This is a ______ .A.a clause of a contract

B.an explanation of a clause in a contract

C.requirement from a government

D.an article of an international convention

At the substituted port, the carrier is entitled to claim ______ if he had dilivered full cargo there.A.full freight

B.half freight

C.no freight

D.reasonable freight

The contract of affreightment is referred to ______ .A.a contract of carriage by which the carrier is entitled to carry certain amount of cargo in a specified time by any vessel or vessels either belonging to himself or to others

B.a contract of carriage, such as Gencon

C.a contract of trade

D.a contract of sales

请帮忙给出每个问题的正确答案和分析,谢谢!

第4题

struct w

{ char low;

char high;

};

union u

{ struct w byte;

short word;

}uw;

main()

{ int result;

uw.word=0x1234;

printf(“word value:%04x\n”,uw.word);

printf(“high byte:%02x\n”,uw.byte.high);

printf(“low byte:%02x\n”,uw.byte.low);

uw.byte.low=0x74;

printf(“word value:%04x\n”,uw.word);

result=uw.word+0x2a34;

printf(“the result:%04x\n”,result);

}

第5题

SUPPLEMENTARY INSTRUCTIONS

1. Calculations and workings need only be made to the nearest RMB.

2. Apportionments should be made to the nearest month.

3. All workings should be shown.

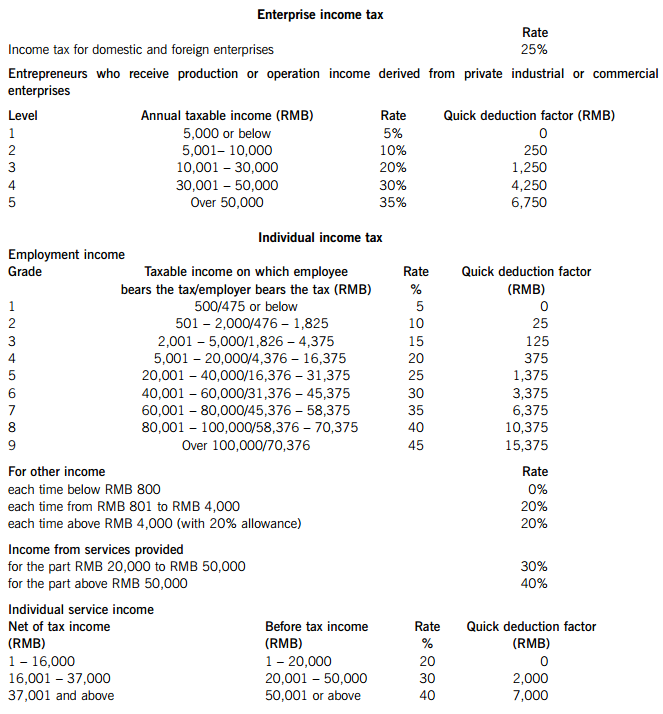

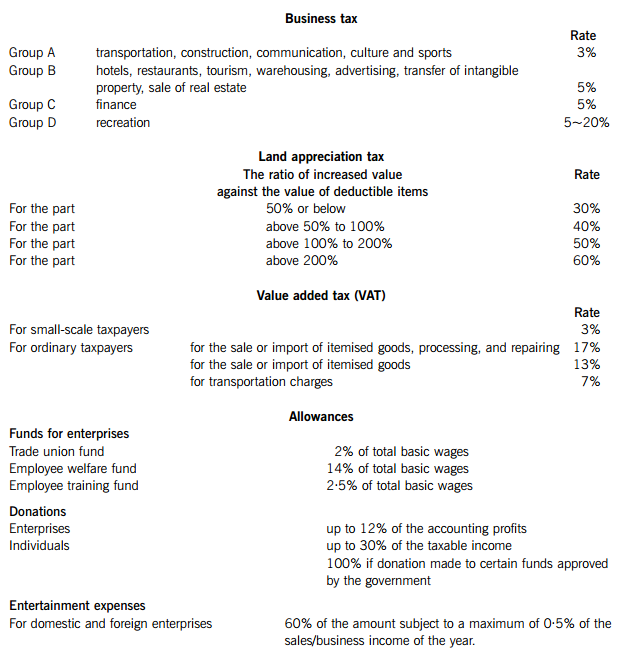

TAX RATES AND ALLOWANCES

The following tax rates and allowances are to be used in answering the questions.

1.

(a) The following is the statement of enterprise income tax (EIT) payable prepared by the accountant of Company P for the year 2010:

Notes:

(1) The union has not yet been set up and the expense is a general provision.

(2) The original cost of the fixed asset was RMB 150,000 and the accumulated depreciation was RMB 105,000, while the accumulated tax allowances claimed were RMB 120,000.

(3) The creditor had been liquidated three years ago.

(4) Last year (2009) was the first year a debtors provision was made. A general provision of RMB 500,000 was made but the whole amount was disallowed by the tax bureau. This year the management decided to write back part of provision amounting to RMB 150,000.

Required:

(i) Briefly comment on the correctness of the accountant’s treatment of the 12 items marked with an asterisk (*) in the income tax calculation sheet; (17 marks)

(ii) Calculate the correct amount of enterprise income tax (EIT) payable by Company P for the year 2010. (6 marks)

(b) Briefly explain the term ‘arm’s length principle’ in the context of transactions between associated enterprises pursuant to the enterprise income tax law, together with the adjustment methods that may be used by the tax bureau in cases where this principle is not complied with. (6 marks)

(c) Company C, a limited company with equity of RMB 1,000,000, borrowed two loans from related companies:

– RMB 1,000,000 at a 7% annual interest rate from Company A; and

– RMB 2,000,000 at an 8% annual interest rate from Company B.

The market interest rate for the equivalent loans is a 6% annual interest rate.

In 2010, the interest paid to Company A and Company B was RMB 70,000 and RMB 160,000 respectively. The total amount of interest of RMB 230,000 was allocated RMB 140,000 to interest expense and RMB 90,000 to construction in progress in Company C’s accounts.

Required:

Calculate the amount of interest that will be disallowed for enterprise income tax under each of the account headings: interest expense and construction in progress. (6 marks)

2.

(a) Mr Y, a local Chinese national, a professional writer and artist, had the following income during 2010:

(1) Received income of RMB 45,000 for publishing the first edition of a book, and of RMB 15,000 for the second edition of the same book. The book was also published in a newspaper and he was paid RMB 5,250 for this.

(2) Sold one of his paintings for RMB 5,400.

(3) Gave a speech and was paid RMB 28,500.

(4) Acted as a translator for a movie and was paid RMB 60,000.

(5) Gave a speech in overseas country M and was paid the gross equivalent of RMB 27,000, from which the equivalent of RMB 6,750 in overseas tax was deducted at source.

(6) Sold one of his paintings in overseas country H, and was paid the gross equivalent of RMB 15,000, from which the equivalent of RMB 2,250 in overseas tax was deducted at source.

(7) Received interest of RMB 7,500 on a loan he had made to a domestic enterprise.

Required:

(i) Calculate the individual income tax (IIT) payable by Mr Y in respect of each of the items (1) to (7); (12 marks)

(ii) State how and when any IIT due on Mr Y&39;s overseas income will be reported and paid. (3 marks)

(b)

(i) State when a withholding agent must report and pay the individual income tax (IIT) deducted on a monthly basis from employment income; (1 mark)

(ii) List ANY FOUR situations in which an individual taxpayer needs to do self-reporting for IIT purposes. (4 marks)

3.

(a) Enterprise G, a general value added tax payer incorporated in Shenzhen for more than 20 years, had the following transactions in the month of May 2010. Some of the enterprises sales are subject to the standard value added tax (VAT) rate, while others are exempt (VAT) activities. All figures are stated including any applicable VAT:

(1) Sold product A (a standard VAT rate item) for RMB 400,000 and product B (a VAT exempt item) for RMB 350,000.

(2) In addition to the sales in (1) above, distributed product A with a market value of RMB 20,000 for staff welfare benefit.

(3) Purchased RMB 500,000 production materials, of which RMB 50,000 was used for a self-constructed building.

(4) Purchased RMB 200,000 agriculture product, of which RMB 20,000 was used for staff welfare benefit.

(5) Purchased a production machine for RMB 100,000 and sold a used machine for RMB 10,000. The used machine had been bought in May 2009 and used by the enterprise ever since then.

Required:

Calculate the value added tax (VAT) payable by Enterprise G for the month of May 2010. (7 marks)

(b) Enterprise H, a small-scale value added tax payer, had the following transactions in the month of May 2010. All figures are stated including VAT:

(1) Sold product for RMB 20,000.

(2) Purchased RMB 500,000 of production materials.

(3) Purchased a production machine for RMB 100,000 and sold a used machine for RMB 10,000. The used machine had been bought in May 2009 and used by the enterprise ever since then.

Required:

Calculate the value added tax (VAT) payable by Enterprise H on each of the above transactions, giving brief explanations of their treatment. (4 marks)

(c) Company X, a property developer, had the following transactions in 2010:

(1) Donated a new building to a high school. The cost of construction of the building was RMB 500,000 and the deemed profit rate is 10%.

(2) Contributed an office building as part of a capital contribution. The cost of the building was RMB 600,000 and the market value RMB 800,000.

(3) Sold an equity holding of unlisted stock for RMB 900,000. The equity holding had been obtained by the contribution of a factory building by Company X which had cost RMB 300,000.

(4) Obtained a six-month bank loan of RMB 2,000,000 from 1 July 2010 with the pledge of a shop owned by the company. During the loan period, the bank did not charge any interest, but instead the bank had the right to use the shop rent free. The market interest rate for a similar loan is 6% per year. At the end of the loan period, Company X sold the shop for a price which gave it RMB 1,000,000 more than the amount needed to repay the bank loan.

Required:

Calculate the business tax (BT) payable by Company X as a result of each of the above transactions (1) to (4), giving brief explanations of their treatment. (6 marks)

(d) State the THREE conditions that must be met for a transportation fee paid by the seller to be excluded from the sale consideration for the purposes of value added tax (VAT). (3 marks)

4.

(a) Company K carried out the following transactions:

(1) Imported a vehicle costing RMB 300,000 and paid transportation costs of USD 10,000 for the journey from the overseas supplier to the port in China.

(2) Shipped a machine with a value of RMB 500,000 overseas for repair and paid for materials of USD 10,000 and a repairing fee of USD 30,000. The machine was shipped back to China in the same month.

(3) Subcontracted some domestic raw materials valued at RMB 200,000 to an overseas company. The related fee and transportation costs were USD 100,000 and USD 20,000 respectively.

(4) Imported raw materials costing RMB 30,000,000 and paid transportation costs of USD 50,000 for the journey from the overseas supplier to the port in China. After the arrival of the materials, Company K discovered that 20% of the materials had a quality problem. The supplier agreed to ship a further 20% replacement materials at no cost to Company K in the same month. Both parties agreed that the quality problem goods should be kept in China.

Required:

Calculate the customs tariff, consumption tax (CT) and value added tax (VAT) payable by Company K as a result of each of the above transactions.

Note: for the purposes of your calculations you should assume that:

(1) The customs tariff for all kinds of imported goods is 20%.

(2) The rate of consumption tax (CT) is 10%.

(3) The USD:RMB exchange rate is 1:6·6

(b) Briefly explain the procedures, including any time limits, for the declaration and payment of the customs

5.

Briefly explain the consequences of the following actions, including any fines or other penalty that may be imposed:

(a) Failure to keep or maintain proper accounting records/vouchers. (2 marks)

(b) Failure to file a return within the prescribed time limit. (2 marks)

(c) Failure to file a return and hence not paying or paying less tax than is duly payable. (1 mark)

(d) Failure to pay tax by concealment of property. (3 marks)

(e) Refusal to pay tax by violence or menace. (2 marks)

请帮忙给出每个问题的正确答案和分析,谢谢!

相关内容

相关内容

下列()不属于中国三大石油公司。A、中国石油天然气集团公司B、中国石油化工集团公司C、中国中化集

国际海洋法庭应对()开放。A、联合国会员国B、所有沿海国C、所有《联合国海洋法公约》缔约国D、所有国

外国船舶在用于国际航行的海峡中,应当享有()的权利。A、科学研究B、水文测量C、过境通行D、勘探开

车站如取消发车进路时,在已开放信号或发车人员已通知司机发车,而列车尚未起动时,车站值班员应先取消发车进路,再通知司机,收回行车凭证()

Q5LSportback后备箱尺寸为同级别最大的520L()

已质押的存单、凭证式国债无论是否已到期,在贷款未全部还清之前,质押物的所有权人或质押物所有人的监护人,不得赎回但可申请挂失止付()

下列()不属于中国三大石油公司。A、中国石油天然气集团公司B、中国石油化工集团公司C、中国中化集

国际海洋法庭应对()开放。A、联合国会员国B、所有沿海国C、所有《联合国海洋法公约》缔约国D、所有国

外国船舶在用于国际航行的海峡中,应当享有()的权利。A、科学研究B、水文测量C、过境通行D、勘探开

车站如取消发车进路时,在已开放信号或发车人员已通知司机发车,而列车尚未起动时,车站值班员应先取消发车进路,再通知司机,收回行车凭证()

Q5LSportback后备箱尺寸为同级别最大的520L()

已质押的存单、凭证式国债无论是否已到期,在贷款未全部还清之前,质押物的所有权人或质押物所有人的监护人,不得赎回但可申请挂失止付()

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!