重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

重要提示:

请勿将账号共享给其他人使用,违者账号将被封禁!

题目

(b) On 1 April 2004 Volcan introduced a ‘reward scheme’ for its customers. The main elements of the reward

scheme include the awarding of a ‘store point’ to customers’ loyalty cards for every $1 spent, with extra points

being given for the purchase of each week’s special offers. Customers who hold a loyalty card can convert their

points into cash discounts against future purchases on the basis of $1 per 100 points. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Volcan for the year ended

31 March 2005.

NOTE: The mark allocation is shown against each of the three issues.

更多“(b) On 1 April 2004 Volcan introduced a ‘reward scheme’ for its customers. The main elemen”相关的问题

更多“(b) On 1 April 2004 Volcan introduced a ‘reward scheme’ for its customers. The main elemen”相关的问题

第1题

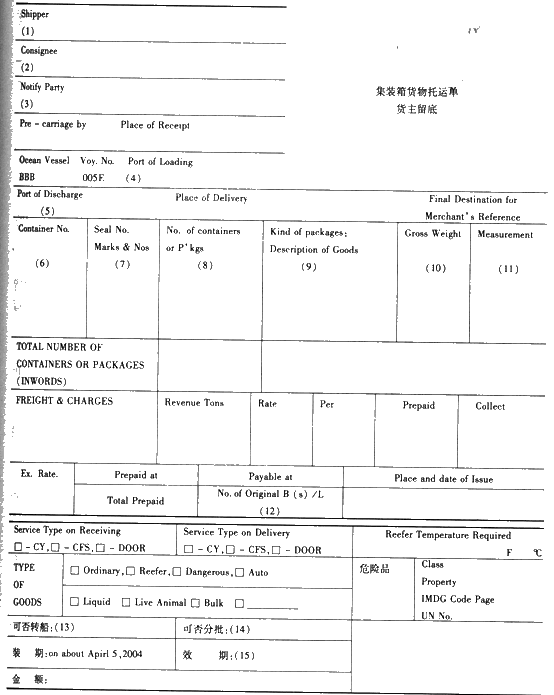

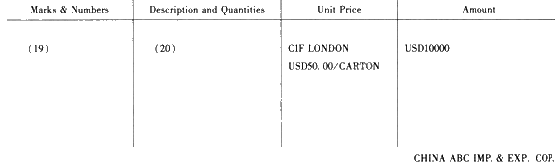

根据下列所提供的信用证条款的主要内容及有关信息,填写集装箱托运单和商业发票

有关项目。

Irrevocable Documentary Credit

Number: LC223 - 5866686

Date: March 5, 2004

Date and place of expiry: April 30, 2004 Qingdao, China

Advising bank: Bank of China

Beneficiary: China ABC Import and Export Corp.

Applicant: U.K. Tom Corp.

Shipment from: Qingdao to London, on or about April 5, 2004

Partial shipments: Not allowed

Transshipment : Not allowed

Description of goods: 100% Cotton Towel as per S/C NO. CH2004

Total amount: USD 10000(SAY US DOLLARS TEN THOUSANDS ONLY)

Total quantity: 200 Cartons

Total gross weight: 20500 KGS

Total. measurement : 30CBM

Price term: CIF London, U.K.

Following documents required:

+ Signed commercial invoice in triplicate

+ Packing list in triplicate

+ Full set of three clean on board ocean bills of lading made out to order of shipper and endorsed in blank and marked "freight prepaid" and notify applicant.

+ Insurance Policy in duplicate for full CIF value plus 10% covering All Risks as per Ocean Marine Cargo Clauses of the PICC dated 1/1/1981 and stating claims payable in London, UK in the currency of the credit.

Information :

Date of Invoice: March 25. 2004

Ocean Vessel: "BBB" Voy. NO. : 005E

B/L NO. : 0128

Container NO. : CBHU0180286

Marks & Nos: CT LONDON NO. 1 -200

Forwarder: China CCC Forwarder CO. (Acting as agent of" the China ABC Import and Export Corp. )

CHINA ABC IMP. & EXP. COP.

18 ZHONG SHAN ROAD, QINGDAO, CHINA

COMMERCIAL INVOICE

To: Invoice Number : ABC2004 - 018

(16) Contract Number:________(17)________

Date of invoice:________(18)________

From________QINGDAO________To________LONDON________

Letter of Credit No. LC123 - 268866 Issued by THE U. K BANK

第2题

4 Assume today’s date is 15 May 2005.

In March 1999, Bob was made redundant from his job as a furniture salesman. He decided to travel round the world,

and did so, returning to the UK in May 2001. Bob then decided to set up his own business selling furniture. He

started trading on 1 October 2001. After some initial success, the business made losses as Bob tried to win more

customers. However, he was eventually successful, and the business subsequently made profits.

The results for Bob’s business were as follows:

Period Schedule D Case I

Trading Profits/(losses)

£

1 October 2001 – 30 April 2002 13,500

1 May 2002 – 30 April 2003 (18,000)

1 May 2003 – 30 April 2004 28,000

Bob required funds to help start his business, so he raised money in three ways:

(1) Bob is a keen cricket fan, and in the 1990s, he collected many books on cricket players. To raise money, Bob

started selling books from his collection. These had risen considerably in value and sold for between £150 and

£300 per book. None of the books forms part of a set. Bob created an internet website to advertise the books.

Bob has not declared this income, as he believes that the proceeds from selling the books are non-taxable.

(2) He disposed of two paintings and an antique silver coffee set at auction on 1 December 2004, realising

chargeable gains totalling £23,720.

(3) Bob took a part time job in a furniture store on 1 January 2003. His annual salary has remained at £12,600

per year since he started this employment.

Bob has 5,000 shares in Willis Ltd, an unquoted trading company based in the UK. He subscribed for these shares

in August 2000, paying £3 per share. On 1 December 2004, Bob received a letter informing him that the company

had gone into receivership. As a result, his shares were almost worthless. The receivers dealing with the company

estimated that on the liquidation of the company, he would receive no more than 10p per share for his shareholding.

He has not yet received any money.

Required:

(a) Write a letter to Bob advising him on whether or not he is correct in believing that his book sales are nontaxable.

Your advice should include reference to the badges of trade and their application to this case.

(9 marks)

第3题

第4题

(c) State any reliefs Bob could claim regarding the fall in value of his shares in Willis Ltd, and describe how the

operation of any such reliefs could reduce Bob’s taxable income. (4 marks)

Relevant retail price index figures are:

September 1990 129·3

April 1998 162·6

December 2004 189·9

第5题

(ii) Write a letter to Donald advising him on the most tax efficient manner in which he can relieve the loss

incurred in the year to 31 March 2007. Your letter should briefly outline the types of loss relief available

and explain their relative merits in Donald’s situation. Assume that Donald will have no source of income

other than the business in the year of assessment 2006/07 and that any income he earned on a parttime

basis while at university was always less than his annual personal allowance. (9 marks)

Assume that the corporation tax rates and allowances for the financial year 2004 and the income tax rates

and allowances for 2004/05 apply throughout this question.

Relevant retail price index figures are:

January 1998 159·5

April 1998 162·6

第6题

(c) In October 2004, Volcan commenced the development of a site in a valley of ‘outstanding natural beauty’ on

which to build a retail ‘megastore’ and warehouse in late 2005. Local government planning permission for the

development, which was received in April 2005, requires that three 100-year-old trees within the valley be

preserved and the surrounding valley be restored in 2006. Additions to property, plant and equipment during

the year include $4·4 million for the estimated cost of site restoration. This estimate includes a provision of

$0·4 million for the relocation of the 100-year-old trees.

In March 2005 the trees were chopped down to make way for a car park. A fine of $20,000 per tree was paid

to the local government in May 2005. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Volcan for the year ended

31 March 2005.

NOTE: The mark allocation is shown against each of the three issues.

第7题

capital of Hira Ltd from Belgrove Ltd. Belgrove Ltd currently owns 100% of the share capital of Hira Ltd and has no

other subsidiaries. All three companies have their head offices in the UK and are UK resident.

Hira Ltd had trading losses brought forward, as at 1 April 2006, of £18,600 and no income or gains against which

to offset losses in the year ended 31 March 2006. In the year ending 31 March 2007 the company expects to make

further tax adjusted trading losses of £55,000 before deduction of capital allowances, and to have no other income

or gains. The tax written down value of Hira Ltd’s plant and machinery as at 31 March 2006 was £96,000 and

there will be no fixed asset additions or disposals in the year ending 31 March 2007. In the year ending 31 March

2008 a small tax adjusted trading loss is anticipated. Hira Ltd will surrender the maximum possible trading losses

to Belgrove Ltd and Dovedale Ltd.

The tax adjusted trading profit of Dovedale Ltd for the year ending 31 March 2007 is expected to be £875,000 and

to continue at this level in the future. The profits chargeable to corporation tax of Belgrove Ltd are expected to be

£38,000 for the year ending 31 March 2007 and to increase in the future.

On 1 February 2007 Dovedale Ltd will sell a small office building to Hira Ltd for its market value of £234,000.

Dovedale Ltd purchased the building in March 2005 for £210,000. In October 2004 Dovedale Ltd sold a factory

for £277,450 making a capital gain of £84,217. A claim was made to roll over the gain on the sale of the factory

against the acquisition cost of the office building.

On 1 April 2007 Dovedale Ltd intends to acquire the whole of the ordinary share capital of Atapo Inc, an unquoted

company resident in the country of Morovia. Atapo Inc sells components to Dovedale Ltd as well as to other

companies in Morovia and around the world.

It is estimated that Atapo Inc will make a profit before tax of £160,000 in the year ending 31 March 2008 and will

pay a dividend to Dovedale Ltd of £105,000. It can be assumed that Atapo Inc’s taxable profits are equal to its profit

before tax. The rate of corporation tax in Morovia is 9%. There is a withholding tax of 3% on dividends paid to

non-Morovian resident shareholders. There is no double tax agreement between the UK and Morovia.

Required:

(a) Advise Belgrove Ltd of any capital gains that may arise as a result of the sale of the shares in Hira Ltd. You

are not required to calculate any capital gains in this part of the question. (4 marks)

第9题

What day is Valentine's Day celebrated? ()

A、Feb.14

B、April 1

C、May 1

D、Jan. 1

第10题

A.$5,976,000

B.$1,524,000

C.$324,000

D.$9,000,000

相关内容

相关内容

发站给中途站预留的包房,可利用其发售最远至预留站的车票()

执勤分队集体外出活动.除当班哨兵外.营区至少保留三班哨的兵力()

骑士小张送餐多了发现有时候顾客不方便出来当面接收货品,小张总结下来觉得送到门卫处/前台/门口等指定的位置后跟客户再三确认是否无误,还得用水印相机拍照通过APP“消息”发给顾客,这样就万无一失了,小张的做法对吗()

新员工入职,按照公司要求到指定医院体检产生的体检费用可自行报销,报销标准为100元/人,报销期限为其入职时间的3个月内()

XT5全系标配EPB电子驻车制动系统()

设备损坏引起水浸,由“谁管理,谁负责”实施,如属自来水公司负责,则由自来水公司负责抢修,物业公司提供协助;如属自管设备,自行组织力量抢修()

发站给中途站预留的包房,可利用其发售最远至预留站的车票()

执勤分队集体外出活动.除当班哨兵外.营区至少保留三班哨的兵力()

骑士小张送餐多了发现有时候顾客不方便出来当面接收货品,小张总结下来觉得送到门卫处/前台/门口等指定的位置后跟客户再三确认是否无误,还得用水印相机拍照通过APP“消息”发给顾客,这样就万无一失了,小张的做法对吗()

新员工入职,按照公司要求到指定医院体检产生的体检费用可自行报销,报销标准为100元/人,报销期限为其入职时间的3个月内()

XT5全系标配EPB电子驻车制动系统()

设备损坏引起水浸,由“谁管理,谁负责”实施,如属自来水公司负责,则由自来水公司负责抢修,物业公司提供协助;如属自管设备,自行组织力量抢修()

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!